Resisting tremendous pressure from the Trump administration, the Federal Reserve held its key interest rate steady on Wednesday as two of President Donald Trump’s appointees dissented from the decision and voted for cuts.

Wednesday’s meeting reportedly marks the first time in more than 30 years that two members of the Fed’s seven-member Board of Governors voted against a rate decision at the central bank.

Vice Chair for Supervision Michelle Bowman and board member Christopher Waller “preferred to lower the target range for the federal funds rate by one quarter of a percentage point at this meeting,” according to the Fed’s policy statement.

In announcing its decision, the Fed said that while economic growth had moderated in the first six months of 2025, inflation remained “somewhat elevated.”

Fed Chair Jerome Powell voted to keep rates unchanged, as did three other board members and the five Fed regional bank presidents who currently sit on the rate-setting Federal Open Market Committee (FOMC). Board member Adriana Kugler was absent from the meeting and did not vote.

Trump has been increasingly incensed by Powell’s refusal to lower rates in recent weeks. At one point, the president was threatening to oust the Fed chairman before his term expires, though the legality of such a plan was unclear. Last week, however, Trump appeared resigned to waiting until next May, when Powell’s four-year term is up, to appoint a new chair.

“I think he’s done a bad job, but he’s going to be out pretty soon anyway,” the president said at an event that aired live on Newsmax and the Newsmax2 free online streaming platform. “In eight months, he’ll be out. But I call him ‘Too Late.’ He’s too late all the time. He should have lowered interest rates many times. Europe lowered their rate 10 times. We lowered ours none, and it’s causing a problem for people that want to buy a home.”

With the Fed’s next meeting scheduled for September, the question now becomes whether the central bank will make cuts then.

“The next two months’ data will be pivotal and we see a path to a resumption of the Fed’s easing cycle in the autumn should tariff inflation prove more modest than expected or the labor market show signs of weakness,” Ashish Shah, a chief investment officer at Goldman Sachs, said in a note to clients after the decision was announced on Wednesday.

Nicole Weatherholtz, a Newsmax general assignment reporter covers news, politics, and culture. She is a National Newspaper Association award-winning journalist.

Treasury Secretary Janet Yellen last week warned that “threats to democracy” will imperil U.S. economic growth. Yellen’s admonishment is a less-than-veiled finger wag at former President Donald Trump and anyone who would dare question the official lie that the 2020 election was “one of the most secure elections in history.”

The real threat to the economy is Joe Biden, his buffoonish treasury secretary, and the rest of the capitalism-crushing useful idiots in this dangerous administration.

As Democrat Party public-relations firm the Associated Press reported, Yellen used “economic data” in her address Friday in Arizona to “paint a picture of how disregard for America’s democratic processes and institutions can cause economic stagnation for decades.”

“Yellen, taking a rare step toward to [sic] the political arena, never mentioned Trump, the presumptive Republican presidential nominee, by name in her speech for the McCain Institute’s Sedona Forum, but she hinted at the former president’s potential impact if he regains the White House,” the AP’s Fatima Hussein and Josh Boak propagandized in a shared byline.

The former Federal Reserve chairwoman, who has routinely injected herself into the “political arena,” used the speech to “serve as a sort of warning for business leaders who may overlook Trump’s disregard for modern democratic norms because they prefer the former president’s vision of achieving growth by slashing taxes and stripping away regulations.”

Yellen’s comments, and the AP article marketing them, are as nakedly political as they are hilariously absurd. Trump’s assertions that the 2020 election was rigged — by shattered election laws in swing states, unprecedented infusions of leftist third-party cash in election administration and election interference by the same rotten-to-the-core corporate media peddling Yellen’s assault on democracy diatribe — are more dangerous than Bidenomics? Americans and economic data disagree.

‘Transitory’ Regret

Yellen’s comments preceded Gallup’s latest Economy and Personal Finance poll showing Americans’ trust in Biden’s leadership at an all-time low. The poll, conducted April 1-22, finds just 38 percent of respondents say they have a “great deal” or a “fair amount” of confidence that Biden would do or recommend the right course for the economy. Former President Donald Trump, the Republican opponent Democrats and their pals in the Deep State are trying to throw in jail, is polling at 46 percent on the economic question.

Understandably, Americans are downright cranky about the shaky state of their personal economy, compliments of the Biden administration’s prosperity-crippling policies.

“With Americans less optimistic about the state of the U.S. economy than they have been in recent months and concern about inflation persisting, their confidence in President Joe Biden to recommend or do the right thing for the economy is among the lowest Gallup has measured for any president since 2001,” Gallup reported Monday.

Over the past three years, Americans learned to be confident that Biden would do the wrong thing. And his bungling treasury secretary has provided plenty of political cover. What is stunning is that a majority of Americans (57 percent) until 2022 had confidence in the Dementarian’s management of the economy. Only President George W. Bush had a lower rating, with a meager 34 percent confidence number at the end of his second term amid the real estate bubble-burst recession.

As inflation began to climb in 2021, economics genius Yellen described the soaring cost of things as a “transitory” problem. She doubled and tripled down as inflation ballooned to levels not seen since the real Great Recession of the 1980s, caused in large part by the policies of a lousy president Biden is often compared to: Jimmy Carter.

“I regret saying it was transitory. It has come down. But I think transitory means a few weeks or months to most people,” Yellen said during an interview with Fox Business in March.

No Sale

Inflation has come up since Yellen expressed her regret. Soaring mortgage rates have priced Americans, particularly young families, out of home ownership. The housing crisis could be the “death knell for America’s middle class,” Newsweek warned in December.

American workers have seen any income growth devoured by rising costs for everything from gas to Happy Meals. Yes, Democrats’ massive expansion of government regulations on business — especially small business, climate change cultism, foreign policy debacles, and unsustainable spending — has everything to do with why middle-income earners are feeling the pain and increasingly frustrated.

Just as frustrating, you have the accomplice media covering for the bungler-in-chief, telling Americans what they’re experiencing is simply not real. The New York Times’ gag-worthy piece last month claiming Biden has a positive story to tell on the economy is political propaganda of the most ludicrous order. No one should be surprised about such absurd water-carrying by a Biden-backing corporate media that has pushed Democrats’ perfect election narrative despite Democrats’ many, many imperfections.

Now the tone-deaf treasury secretary wants to tell American businesses that tax-cutting, “election denier” Trump is more of a threat to the U.S. economy than the economic menace that is Joe Biden. America isn’t buying what Yellen is selling. They can’t afford to.

Matt Kittle is a senior elections correspondent for The Federalist. An award-winning investigative reporter and 30-year veteran of print, broadcast, and online journalism, Kittle previously served as the executive director of Empower Wisconsin.

U.S. Federal Reserve Chair Jerome Powell attends a press conference in Washington, D.C., on March 20, 2024. The U.S. Federal Reserve on Wednesday left interest rates unchanged at a 22-year high of 5.25% to 5.5% as recent consumer data indicates continued inflation pressures. (Photo: Liu Jie/Xinhua via Getty Images)

In 1913, Woodrow Wilson and his progressives promised that the Federal Reserve would avert both depressions and inflation, while preventing the wealthy from controlling America’s financial markets at the expense of the poor.

More than a century later, it’s clear that was all a lie, and the Fed has helped create a permanent American underclass.

The Fed was designed to transfer wealth from the American people to the government, mostly through the hidden tax of inflation. But this process has prevented countless American families from being able to save and get ahead, because their savings are constantly losing value.

For two decades, the Fed kept interest rates artificially low to help finance massive government spending. When that spending reached unprecedented heights in 2020, the Fed intervened more drastically than ever, creating trillions of dollars and devaluing the currency.

Thus began an unparalleled transfer of wealth that continues to this day, and which has driven a wedge between different groups of Americans.

The painful inflation of the last three years has increased prices throughout the economy, distorting the signals that prices are supposed to convey to buyers and sellers. For example, the cost to own a median-price home today has doubled since January 2021, but it’s still the same house.

This phenomenon represents the monetization of housing, where a dwelling becomes a much better store of value than the currency, even if the real value of the house hasn’t improved.

Likewise, Americans’ earnings have increased substantially over the last three years, but not in the most meaningful sense — that is, what they can buy. Instead, the opposite has happened, and today’s larger incomes buy less.

What would have been a decent salary in 2019 is no longer enough to even get by in many places, and it’s certainly not enough to ever fulfill the American dream of homeownership.

A family earning the median household income can afford a median-price home in only a handful of major metropolitan areas in the entire country. In many cities, the cost to own a median price home exceeds the take-home pay from the median household income. Even if you didn’t spend a dime on other necessities such as food, you still wouldn’t have enough for your mortgage payment.

It’s truly a condemnation of the status quo when even those with seemingly high incomes cannot afford a typical house.

Worse, as prices continue marching upward, people can save less, making it harder to accrue a sufficient down payment. Even by the time a family reaches their goal, home prices have increased again, and they’re back on the hamster wheel, trying to save for an even larger down payment.

Meanwhile, inflation is steadily, though silently, taxing away the real value of the family’s savings as they sit in the bank.

This has left countless Americans as perpetual renters, with almost an entire generation of young people giving up on having the standard of living that their parents had. An artificial chasm has been constructed between those who already own capital, like housing, and the remaining Americans who can only borrow such assets, as they do by renting.

Similarly, many of those struggling to afford sharply increased rents are going deeply into debt to keep a roof over their head while those who locked in a mortgage with a fixed interest rate before both home prices and interest rates exploded have shielded themselves from one of the largest drivers behind the cost-of-living increases of the last three years.

Many homeowners could not afford to buy their same home today. The monthly mortgage payment on a median-price home has doubled since January 2021. Thus, even if two families have identical incomes, the one that bought a home three years ago has a nearly insurmountable advantage over the other family trying to do so today.

The Fed‘s monetary manipulations have financed trillions of dollars in federal budget deficits, but they’ve also created a permanent American underclass, something antithetical to the Founders’ vision for the country.

Class mobility is at the heart of the American dream, and the Fed has turned it into a nightmare.

In July 1944, 44 delegates from Allied countries came together during World War II in Bretton Wood, New Hampshire. The goal? Devise an international currency system to manage foreign exchange that would disadvantage no country and effectively facilitate post-war rebuilding and commerce. The outcome: The U.S. greenback would be the world’s reserve currency.

It has been almost 80 years since, and all nations have been better off with a United States dollar-dominated world. World gross domestic product (GDP) in 1940 was $7.81 trillion. For 2023, the world GDP is expected to be $112.6 trillion. That is an increase of 1,441 percent. Billions of people have been lifted out of poverty because of this.

China is working overtime to disrupt the dollar-dominated world economy. The significance of the dollar losing its premier position cannot be overstated. The Biden administration should not overlook this.

Most Americans may be unaware of crucial transactions occurring around the globe recently. And who could blame them? All the corporate media’s main headlines have been over the now-public indictment of former President Donald Trump, over factually weak allegations involving hush-money payments to a porn star.

The indictment of a former president is a crossing-of-the-Rubicon moment in American history. But displacing the dollar as the world’s reserve currency, as China and Russia have both made known is their objective, has analogous ramifications for the world. But while the world watches Trump’s indictment, they are missing China’s transactions with some of our major allies and trading partners in the yuan. Notably, China is doing this with nations that need better stewards.

Bloomberg News reported in February 2023 that the Inevitable Rise of the Petroyuan (yuan used to settle Middle East oil transactions) was a “myth.” One month later, Saudi Arabia and OPEC are now considering just that.

In our republic, the founders “separated the purse from the sword.” With the passing of the Federal Reserve Act of 1913, Congress further separated the purse from our elected representatives by giving the Federal Reserve power over the nation’s money supply.

China has no such separation of powers. President Xi Jinping wields both the sword and purse. What that means if the yuan were to become the global reserve currency is giving the Chinese Communist Party effective control over the money supply for the entire world. The United States would still have the dollar, but it would require exchanging for the yuan to transact with other nations.

Inflation and deflation can both have devastating effects on the economy. Deflation is what caused the Great Depression. Inflation, as we all feel the pain currently, caused an entire decade to be lost in the 1970s.

Allowing China to become the facilitator of the currency used in global commerce, such as the dollar is now, would be to give unprecedented powers to a communist dictatorship. The ebbs and flows of the global economic apparatus would be subject to a hostile foreign power that has no issue retaliating against other sovereign nations that disagree with them.

If the Chinese yuan were to become the global reserve currency, it would, in essence, give the CCP the ability to cripple entire nations. With a country as hostile as China, entire sovereign nations would be subject to the whims of the communists who run their countries. The CCP could arbitrarily restrict credit, enact sanctions, block entire nations from global commerce vis a vis foreign exchange prohibition, and use any of the other vast economic warfare tools the global reserve currency brings. Of course, unless nations decide to toe the Communist Party line.

The world would be like when we were younger and our financial life was dependent upon allowances given to us by our parents. Except in this case, instead of doing chores, nations would have to accept genocide, persecution of minorities, and the desecration of civil rights. We can bet governments would likely have to become complicit. That is not out of the realm of possibility when dealing with actors such as communists.

Mackenzie Alan Bettle graduated from Arizona State’s W.P. Carey School of Business with a bachelor’s in business, law, and economics, summa cum laude, and received his Juris Doctorate from Seton Hall University Law School with an emphasis on law and economics. He is a practicing attorney in Phoenix, Arizona. He loves business, politics, economics, law, football, and his two fluffy Havanese dogs, Jack and Kobe.

It’s painful for me to watch so many smart pundits and politicians on both the right and the left buy into a media narrative that seeks to blame “wealthy speculators” or “tech bros” or venture capitalists for a banking crisis that ultimately started in Washington. Let me explain.

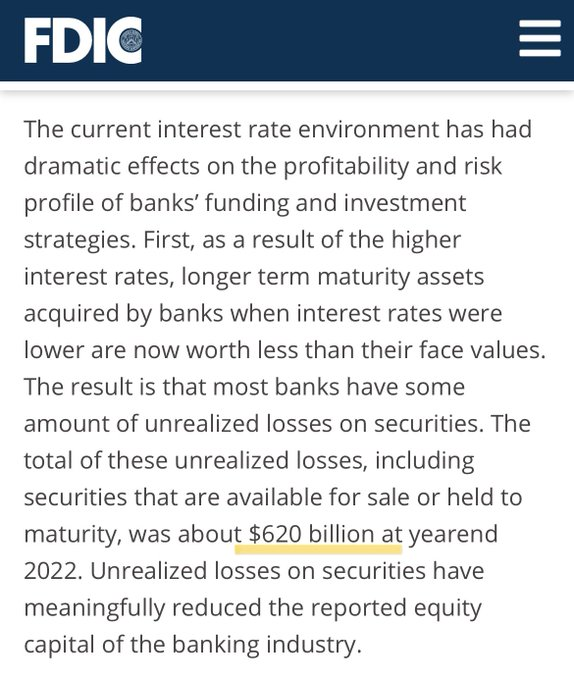

If you want to understand the context for the crisis, look at the Federal Deposit Insurance Corporation chair’s March 6 testimony — a week before Silicon Valley Bank’s collapse — where he explains that banks were sitting on $620 billion of unrealized losses from long-dated bonds. This provided the tinder for the crisis.

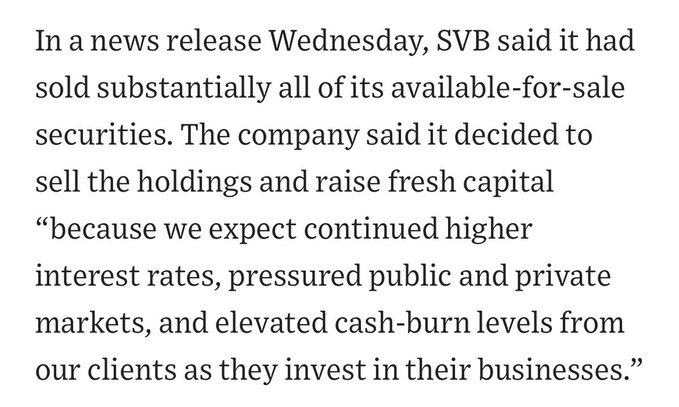

The match was lit when SVB announced on Wednesday, March 9, that it had effectively sold all of its available-for-sale securities and needed to raise fresh capital because of large unrealized losses from its mortgage bond portfolio.

Screenshot: Wall Street Journal

On Thursday morning, the financial press widely reported SVB’s need for new capital, and short sellers were all over the stock. The CEO’s disastrous “don’t panic” call later that morning only heightened fears and undermined confidence in the bank.

The idea that one needed “non-public information” to understand that SVB was at risk is drivel being peddled by populist demagogues. Any depositor who could read The Wall Street Journal or watch the stock ticker could understand there was no upside in waiting to see what would happen next.

By Friday, the run on other banks had begun. This became abundantly clear when regulators placed Signature Bank in receivership, announced a backstop facility for First Republic, and temporarily halted trading of regional bank stocks on Monday. Even trading of Schwab was halted.

Some unscrupulous reporters and political types have even claimed that I somehow caused this through my tweeting. Dang, they must think I’m Superman! Or maybe E.F. Hutton. But the timing doesn’t line up at all, as I already explained.

In the never-ending quest for scapegoats, some reporters and political types are asking if @theallinpod could have influenced the bank run. We didn't publish until Saturday morning when banks were already closed! I also never tweeted about SVB until it was already in receivership…

Once the run on the bank started, decisive action by the Fed was imperative. This meant protecting deposits (uninsured are 50 percent) and backstopping regional banks. No matter how distasteful you may find those things to be, preventing a greater economic calamity was necessary.

But back to SVB: Its collapse was first and foremost a result of its own poor risk management and communications. It should have hedged its interest rate risk. And it should have raised the necessary capital months ago through an offering that didn’t spook the street.

SVB doesn’t deserve a bailout and isn’t getting one. SVB’s stockholders, bondholders, and stock options are getting wiped out. The executives will spend years in litigation and may have stock sales clawed back. Anyone who thinks there’s a “moral hazard” isn’t paying attention.

But it’s important to understand that SVB’s failure didn’t arise from risky startups doing risky startup things. It arose from SVB’s over-exposure to boring old mortgage bonds, which were considered safe at the time SVB bought them. Perhaps this is why SVB had an “A” rating from Moody’s and had passed all of its regulatory exams.

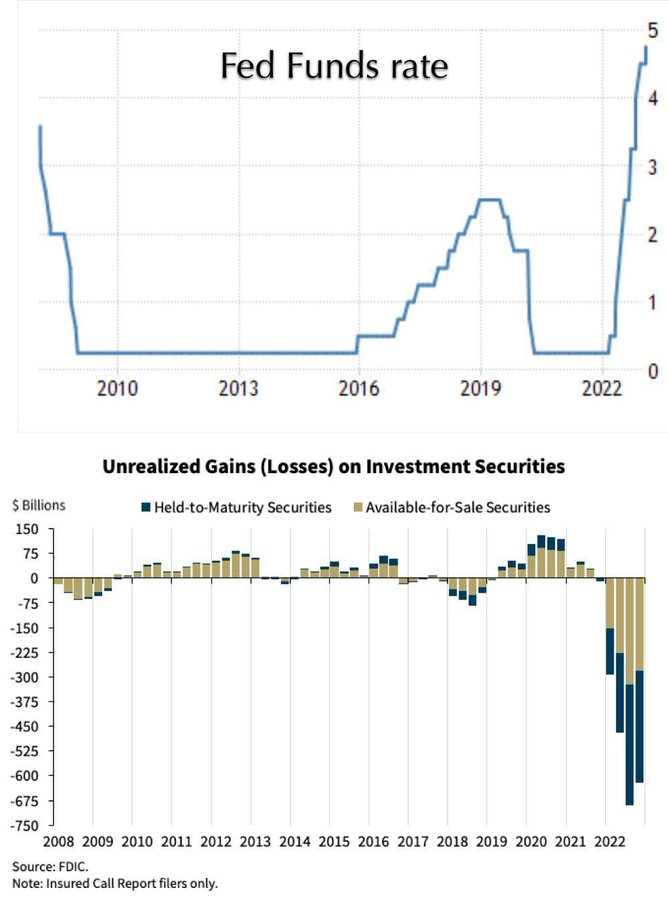

What turned the mortgage bonds toxic? The most rapid rate-tightening cycle we’ve seen in decades. You can see the connection here between rapid rate hikes and unrealized losses in the banking system.

So, what caused the rapid rate hikes? The worst inflation in 40 years. And what caused that? Profligate spending and money printing coming out of Washington — all while Joe Biden, Janet Yellen, and Jerome Powell assured us inflation was “transitory.”

I warned two years ago that pumping trillions of dollars of stimulus into an already hot economy was an unprecedented and likely dangerous experiment. But this was Bidenomics.

Bidenomics = pumping trillions of dollars of stimulus into a rip-roaring economy. I’m not going to pretend like I know what’s going to happen next. AFAIK we’ve never tried this before.

So, when Joe Biden says he’s going to hold those responsible for this mess fully accountable, he ought to start by looking in the mirror. But I’m sure that’s not going to happen, just as I’m sure the hunt for scapegoats is just beginning.

David Sacks is an entrepreneur and author who specializes in digital technology firms. He is a co-founder and general partner of the venture capital fund Craft Ventures and was the founding COO of PayPal.

Like Blaze News? Get the news that matters most delivered directly to your inbox. SIGN UP

We have no free market and never will have one so long as the Federal Reserve exists in its current form. It is the unelected judge, jury, and executioner of the economy that can pick winners and losers by manipulating credit and monetary policy to artificially inflate certain investments and investors at the expense of others. Years of unnaturally low interest rates have enriched well-connected woke elites at the expense of consumers and savers. Now that their Ponzi scheme is coming due, with the collapse of one of the wokest banks and the vicious cycle of stagflation and reliance on loose money, it’s time for conservatives and GOP presidential candidates to revisit the idea of either abolishing or severely limiting the role of the Fed.

For the past several generations, the Democrat Party thrived on class warfare. Democrats claimed that conservatives elevated the wealthy at the expense of the working class simply because they didn’t support free stuff and redistribution of wealth through an extremely progressive income tax on legitimately earned wealth. But it turns out that their policies have actually artificially enriched the wealthy and harmed middle-income consumers and savers, but unlike with our policies, the wealthy never earned these tendentious favors, nor are they constitutional.

In many respects, the Federal Reserve has more power than all three branches of government put together, yet the members never stand for reelection. For years, the Federal Reserve has created endless inflation and loose credit with near-zero interest rates and by buying up trillions of dollars of securities and treasuries. It distorted the market, allowed woke banks like Silicon Valley Bank to overextend themselves, and even become the primary lender for solar financing in America, based on Monopoly money.

Now that the Fed inevitably was forced to hike interest rates to curb some of the historic inflation it helped create, Silicon Valley Bank, along with Signature Bank in New York (the bank Barney Frank joined when he left Congress), collapsed and was taken over by the FDIC. But just like a frustrated teen losing a video game, the Federal Reserve and the Treasury Department are pulling the plug on the game so that their buddies don’t lose. Remember, until Friday, SVB’s CEO, Gregory Becker, was on the board of directors at the San Francisco Fed. It’s one big game of, by, and for the politically connected venture socialists.

Less than 10 hours after Treasury Secretary Janet Yellen promised there would be no new bank bailout, the Federal Reserve issued a statement Sunday evening announcing a spectacular bailout of every penny of deposits both at SVB and at Signature Bank. Except this one, unlike in 2008, won’t even require a vote in Congress, because the Federal Reserve and the Treasury Department have the backhanded tools to print money, even though we have reached the statutory debt limit.

“The financing will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral,” wrote the Fed. “These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

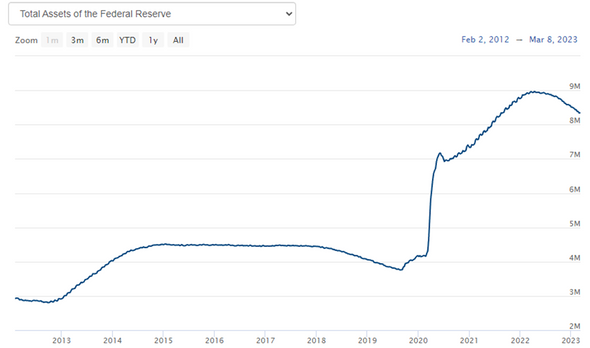

In other words, they are back to printing money. The Fed has already grown its balance sheet by $4.7 trillion during the frenetic COVID money-pumping scheme (in addition to Congress’ $5.5 trillion fiscal stimulus), and has only off-loaded roughly $600 billion over the past year.

This was after many preceding years of ultra-loose monetary policy. Finally, as inflation reached record highs last year, the Fed began to ease up on those policies. Not any more! The Fed is promising to buy the assets “at par,” not at market value, which will have the effect of loosening bank credit beyond belief.

Additionally, along with the Treasury Department, the Fed will make $25 billion available as a backstop to this quantitative easing scam. The debt limit is a complete mockery, because evidently the Treasury Department can come up with vast sums of money on the fly, and this is likely the tip of the iceberg. Once the initial shock of this policy sets in, the debate will merely be over how many hundreds of billions are offered to stem the panic from other banks.

The immediate effect of this bailout will be to halt all interest rate hikes. As of this morning, the yield on the two-year Treasury note was down more than 80 basis points since last week, in anticipation of the return to loose credit. So the government will crush consumers with record inflation to bail out the well-connected woke (ESG-supporting) elites who took advantage of the unnatural and manipulated easy credit. John Edwards was indeed correct that there are two Americas, except it’s not because of a lack of government involvement. It’s because of too much big government, and particularly an unelected fourth branch of government that should be abolished.

If it’s impractical to immediately abolish the Federal Reserve, we should at a minimum remove its power to serve as both the arsonist and the firefighter. Congress must repeal the Humphrey-Hawkins bill from 1978, which empowers the Fed with a “dual mandate” to achieve maximum sustainable employment and keep prices stable. The Fed should be forced to focus solely on price stability. This would take “the game” out of the Fed. If it has no ability to create stimulus and provide monetary morphine, Wall Street can’t anticipate it and build an artificial economy based on its nourishment.

Market-distorting monetary manipulations are no different from market-distorting fiscal policy from the government. This is how the statists have successfully dissuaded us from ever limiting government. “You really plan to pull the rug out from under such-and-such industry?” the forces of special interests groan, be it health care or the financial sector. The same applies to monetary policy. There is no reason why we should allow the Fed to use monetary stimulus in such an officious manner that the entire market would collapse without the monetary morphine, even during robust economic growth.

The Fed should also be banned from buying up other securities and bonds, such as mortgage-backed securities from Freddie and Fannie. We must stop distorting the markets by encouraging investments on the basis of how much capital is available instead of real growth in a specific industry. It’s time to go back to the days of real economic growth built on the fiscal equivalent of protein and healthy fats, not sugar and carbs for the well-connected elites involved in regulatory capture.

We have enough lawless, unelected branches of government. It’s time to stop creating asset bubbles and misallocation of resources and return to a true organic equities market that reflects the economic realities of America. That will not happen until the Fed is brought under the checks and balances of the republic. As Andrew Jackson warned of a central bank, “The bold effort the present (central) bank had made to control the government … [is] but premonitions of the fate that awaits the American people should they be deluded into a perpetuation of this institution or the establishment of another like it.”

Arecession is coming in 2023, concluded more than two-thirds of the economists at big financial institutions recently surveyed by The Wall Street Journal. Inflation is also likely to remain high. Measuring year-over-year inflation by the U.S. government’s 1980s methodology put it at 15.23 percent in November 2022 instead of the government’s claimed 7.11 percent, according to economist John Williams.

Many commentators, including me, were wrong when we previously claimed our grandkids will be paying off America’s massively unaffordable welfare state. We are all paying for it right now and are likely to be for much of our lives in inflation and other economic devastation.

Nobel Prize-winning economist Milton Friedman’s maxim that “inflation is always and everywhere a monetary phenomenon” — meaning, inflation is always caused by government overspending — predicts continued inflation for at least the next five years, if not longer.

That’s because government entities are continuing to engage in seriously inflationary actions. They’re doing this partly because of ideology, partly to buy votes, and partly because they prefer eating away Americans’ savings to paying off the unprecedented government debt that politicians have accumulated in the last 70 years enriching their friends and buying off voters.

Inflation Means Politicians Stealing from You

A 2021 Politico profile of a former U.S. Federal Reserve member noted, “Between 2008 and 2014, the Federal Reserve printed more than $3.5 trillion in new bills. To put that in perspective, it’s roughly triple the amount of money that the Fed created in its first 95 years of existence. Three centuries’ worth of growth in the money supply was crammed into a few short years.”

That dissenting former Federal Reserve committee member, Thomas Hoenig, “was worried primarily that the Fed was taking a risky path that would deepen income inequality, stoke dangerous asset bubbles and enrich the biggest banks over everyone else,” the profile says. “He also warned that it would suck the Fed into a money-printing quagmire that the central bank would not be able to escape without destabilizing the entire financial system.”

Essentially, the Federal Reserve has been helping Congress manufacture money to buy up the public debt they contracted by promising Americans more stuff than we can pay for. That’s been ongoing since the 1960s Great Society, which basically paid Americans with unaffordable entitlements to shut up about the steady loss of their constitutional freedoms, according to scholar Christopher Caldwell.

The Borrowing Will Go On Until It Can’t

In 2021, 41 percent of federal spendingdependedon borrowing. In 2022, 22 percent did. This means raising the cost of debt by hiking interest rates, as the Fed is now doing, could provoke a crisis because it would make Congress’s unsustainable behavior even more painful.

As a Manhattan Institute analysis by economist Brian Riedl notes, “rising interest rates risk pushing government interest costs, annual budget deficits, and total government debt to unsustainable levels … once the debt surges, even modest interest-rate movements can impose stratospheric costs.”

This would call years of government bluffing about the state of federal finances and institutions. It would require Congress not only to stop spending but to cut programs, which means angering voters. It would usher in the unavoidable and painful new era of managing America’s decline.

“Once a debt-and-interest-rate spiral begins, it is nearly impossible to escape without drastic inflation or fiscal consolidation,” Riedl notes.

However this ends, it is likely to include a lot of economic pain, one way or another. Here are just a few of the many indicators that inflationary times are not going away fast.

1. ‘Covid’ Overspending Continues Until at Least 2024

The funds for the sixth waste-packed “Covid relief bill” will be distributed to big-government donors, states, and local governments through the end of presidential election year 2024. Yes, the American Rescue Plan Act from Covid-tide sends states and local governments $350 billion that is still being rolled out — by design.

That law’s total spending comprises more than 100 times states’ 2020 budget shortfalls, and many state and local governments can hardly figure out what to do with all the money. As they take years to spend it, that money will keep juicing inflationary pressure. A similar effect is occurring with all the so-called Covid relief bills, which together sent $6 trillion spinning through the economy, devaluing our currency. Much of this wild inflationary deficit spending has been electronically printed through the Federal Reserve.

Together, 2020s federal spending allegedly in response to Covid was more than double the inflation-adjusted federal response to the 1930s Great Depression. We’re already seeing the inflationary effects of all this so-called Covid spending, and it’s not over yet.

2. Democrats and Republicans Recently Went on Even More Inflationary Spending Binges

In conjunction with Democrats’ mega-spending “infrastructure” and “green energy” bills soon after Covid that also helped them win Congress and the presidency in 2020, all this extra spending is projected to increase the federal debt by an unprecedented $6.5 trillion, costing more than the 20 years of U.S. occupation of Iraq and Afghanistan, according to Riedl.

“In other words, the U.S. government is in the early stages of what is projected to be the largest government debt binge in world history,” Riedl notes.

That doesn’t even include the massive federal spending expansions to support a large army of grifters profiting off the human suffering of the Russia-Ukraine war in 2022. Congress spent more on the first four months of Ukraine’s war than it did on the first five years of its undeclared war in Afghanistan.

Atop all this, more deficit spending is likely to come. In August 2022, Democrats confirmed yet again that historic levels of inflation that year were no impediment to their big-spending aims when Biden announced that he’d force taxpayers to assume up to nearly $1 trillion in student loans taken on by largely higher-income professionals. That spending is tied up in court and could be allowed at any time.

This all means that the source of inflation — government overspending — is at an unprecedented rate and pace, and even with the House Freedom Caucus’ negotiated limits on congressional spending activity, trillions in new spending is already locked in.

3. Build Back Bankrupt Shoveled Yet More Out the Door for Years to Come

In 2022, the Biden administration managed to get its top-priority grab-bag of increased government spending signed into law. By spending more money the government does not have and imposing more taxes, the ridiculously named Inflation Reduction Act is likely to increase inflation, said a Tax Foundation analysis.

“By increasing spending, the bill worsens inflation, especially in the first four years, as revenue raisers take time to ramp up and the deficit increases,” the foundation’s analysis says. “We find that budget deficits would increase from 2023 to 2026, potentially worsening inflation.”

Continuing to shovel money to cronies while ignoring major structural problems in the U.S. economy and federal budget process has become a hallmark of Congress in the 2000s. This has to end at some point, but until that point comes reasonable people can only expect such legislation to continue to pass, and to continue to worsen inflationary pressures.

Given how reckless both parties have been for decades on fiscal matters, it is likely this norm of spending money Congress can’t actually appropriate will continue until a major disaster ends their ability to fake.

4. Federal Officials Are Destroying the People’s Trust

Inflation happens “When money is no longer a trustworthy measure of value,” note Steve Forbes, Nathan Lewis, and Elizabeth Ames in their 2022 book, “Inflation.” Inflation is at least partly about a crisis of confidence in government — a warranted one, usually, because major inflation occurs as a result of politician malfeasance. Unfortunately, U.S. government officials are doing nothing to restore the people’s lost confidence in them — in fact, just the opposite.

In 2022, federal officials spent months denying inflation was happening. They also denied the United States was in a recession, insisting the traditional definition of two economic quarters in contraction was false when it was applied under Democrat rule. They’ve switched how they measure inflation to hide a large part of it.

U.S. leaders also refuse to stabilize our currency, instead taking actions that further erode Americans’ ability to put food on the table and get ahead through legitimately productive honest labor (as opposed to bullsh-t jobs). This does the opposite of what is needed: restore confidence in our markets by announcing strong steps to strengthen the U.S. dollar. They are also engaging in other activities that only erode confidence in the U.S. financial system, such as monetizing the federal debt and refusing to stop massive deficit spending.

Because politicians have created this situation and keep refusing to actually address it, Americans increasingly don’t trust their government or our debt-driven financial system. Polling shows public trust repeatedly hitting new record lows for every social and political institution. That’s an economic problem as well as a political and cultural problem, because a lack of confidence in markets can trigger economic growth, recession, and panics.

Usually, such crises build under the surface for a long time and then burst out into the open all of a sudden. As Hoover Institution economist John Cochrane said during a panel discussion, “Debt crises are like the Spanish Inquisition; no one expects them to come. If you knew they were coming, they would have already happened.”

5. The U.S. Federal Government Is Effectively Bankrupt and Inflation Helps It Hide That

The on-books U.S. national debt of $31.5 trillion is just the tip of the iceberg. Our entitlement systems are about to start going bankrupt, adding trillions in additional financial burdens on taxpayers. Riedl notes, “The U.S. government is projected to run a staggering $112 trillion in budget deficits over the next three decades, driven mostly by Social Security and Medicare commitments that are already set in law.”

If one adds unfunded and other liabilities that government officials keep off the books such as Federal Reserve debt, the amount the U.S. national government owes is more than $200 trillion. That doesn’t include what state and local governments owe, and many of them are also bankrupt or getting there.

“No matter what interest rate you use, the U.S. needs to immediately and permanently raise every federal tax by at least one third to pay, through time, for what our government plans to spend,” Boston University economist Laurence Kotlikoff wrote with fellow economist John Goodman in 2021. “The alternative? Massive spending cuts. And, no, the Federal Reserve can’t make this problem go away by printing the money needed by the Treasury. This would end where it always does — in hyperinflation.”

U.S. debt, deficits, and unfunded liabilities — which together form a total picture of U.S. national economic entrapment — are the largest ever measured in world history. Besides Japan, which isn’t spending the majority of its debt on entitlements like the United States is, “Greece and Italy are the only other OECD countries with a total government debt exceeding that of the United States,” Riedl notes. Greece and Italy have had major sovereign debt crises that have destroyed their standards of living and brought their economies into long-term decline.

“When you look at these numbers, you realize we’re Argentina in 1910,” Kotlikoff told CNBC in 2018, before the alarmist Covid response and Biden presidency made things much worse. All it will take for these scary structural problems to become visible and impossible to ignore is a financial panic or another major event like a war. Oh, look, Congress is also pushing us ever-toward open war with Russia instead of toward peace. Brilliant.

6. Child Scarcity Will Drive Higher Prices

In March 2022, The Wall Street Journal reported the opinion of retired British central banker Charles Goodhart that global structural factors will drive higher inflation for years to come. Goodhart helped Prime Minister Margaret Thatcher break inflation in the 1980s. He told the Journal that the rising global crisis of child scarcity will also push inflation up for decades.

As labor becomes more scarce, he maintained, workers will push for higher wages, in turn driving up prices. At the same time, businesses will manufacture and invest more locally to help offset both labor shortages and the nationalist and geopolitical pressures curbing globalized supply chains. That will increase production costs and local workers’ bargaining power. Global savings will fall as older people consume more than they produce, spending particularly on healthcare. All that will push up interest rates, he predicted.

A meeting of global central bankers in Jackson Hole, Wyoming, in August 2022 for the first time since 2019 found the bankers publicly reflecting a similar assessment, the Journal reported. “I don’t think that we are going to go back to that environment of low inflation,” European Central Bank President Christine Lagarde said on a panel.

7. The People Who Did All This Are Still in Charge

This reality applies to nearly every major political problem: The same people who have created these messes are the same people who largely retain the power to respond to them. The same people writing massive spending bills that divert our economy away from productive labor and into rent-seekers’ pockets are still largely in charge of government spending.

There might have been a slight shift of power in the House, but there hasn’t in the Senate, nor in the presidency. The same guy who claims the power to “pen and phone” a trillion dollars in student loan bailouts is in office, and all his K Street and Wall Street buddies still have gleefully effective access. You can be sure this cabal of crooks isn’t going to be looking out for your best interests now that we’re about to have a potentially dangerous recession.

That may be the most significant systemic reason to expect our markets to be heading for an even rougher ride in 2023 than we’ve had from 2020 to 2022.

The Federal Reserve announced an interest rate hike of 0.75 percentage points, bumping the range of the federal interest rate to between 3.75% and 4% following a Wednesday meeting of Fed policymakers. The rate hike matches investor expectations and is the fifth consecutive hike since March and the fourth at this aggressive pace since June as the Federal Reserve attempts to cool the economy and blunt persistently high inflation, The Wall Street Journal reported Tuesday. All eyes are now on the Fed’s December meeting, with investors debating whether the Fed will continue at its aggressive pace of 0.75 percentage point hikes or slow to 0.5 in a bid to ease the pressure on an economy an emerging consensus of analysts say is heading towards a recession. (RELATED: European Central Bank Takes Action As EU Teeters On Brink Of Recession)

Some investors were hoping the Fed would begin a “pivot” towards reduced rate hikes in December after various signs that the economy was beginning to slow, Reuters reported Tuesday. However, following a Bureau of Labor Statistics report Tuesday that showed an unexpectedly strong labor market, with job openings in September nearly recouping an August decline, some investors believe the Fed will likely see itself as having more work to do in prompting a slowdown.

“Despite other signs of economic deceleration,” Ronald Temple, head of U.S. equity at financial advisory firm Lazard Asset Management, told Reuters, “the job openings data taken together with nonfarm payroll growth indicate the Fed is far from the point where it can declare victory over inflation and lift its foot off the economic brake.”

The Fed is expected to raise interest rates again today by .75% in a poor attempt to curb inflation. Meanwhile oil companies have reported over $50 billion in third quarter profits exceeding expectations. Corporate greed is driving inflation.

So-called “core inflation,” which measures inflation less food and energy, ticked up to 5.1% year-on-year in September, according to the Fed’s preferred inflation metric, the Personal Consumption Expenditures (PCE) price index. The more well-known Consumer Price Index (CPI) has repeatedly come in hot, with its most recent reading also showing soaring core inflation, up 0.6% on a monthly basis in September and up 6.6% on an annual basis.

Heightened rates have pushed people away from buying houses at the fastest rates on record, as 30-year fixed mortgage rates hit their highest levels in 20 years. Elevated interest rates are also putting pressure on the federal government, with the cost of interest on the $31.1 trillion national debt set to surpass the $750 billion spent on defense this fiscal year by 2026, according to CNN.

Why have investors been restricted in buying GameStop shares?

The stock market closed out a week of intense losses with the Dow Jones falling more than 750 points Friday, entering bear market territory amid a wave of investor fears.

At time of writing, the index had, at its lowest point, fallen more than 2.7% during the day to around 29,300 points, with the Nasdaq and S&P 500 down by 2.7% and 2.64% respectively at time of writing. With the Dow Jones officially falling more than 20% from its recent peak in June, stocks will have entered a slump known by investors as a “bear market” if the losses hold when trading ends Friday, according to CNBC. (RELATED: Stocks Stay Volatile As Recession Fears Loom)

The Nasdaq was down by 30.92% this year, with the S&P 500 down 22.98% this year, as of close of business yesterday, according to data from MarketWatch.

“Stocks were overvalued because their nominal price has been fueled by the inflation of the Federal Reserve,” Heritage Foundation economist E.J. Antoni told the Daily Caller News Foundation. “As soon as the Fed took away the punch bowl… what happened? Stocks immediately took a nosedive and are continuing to do so, because the only thing that has been fueling this economic recovery hasn’t been real growth, but again, money creation.”

This Great Bond Bear Market is "thus far a doozy," with the worst losses since 1949, 1931 & 1920: BofA's Hartnett. This "threatens credit events & liquidations of the most crowded trades," long dollar, PE, big tech. "True capitulation is when investors sell what they love & own" pic.twitter.com/R3CSUXTJNo

After wavering early this week as investors awaited the Federal Reserve’s Wednesday announcement of a third interest rate hike in just four months, stocks tumbled, with Goldman Sachs warning clients that investors are preparing for recession and slashing its expectations for the S&P 500 stock index by 16%.

Federal Reserve Chair Jerome Powell has been clear that he is willing for there to be some economic “pain” in order to combat inflation, even as the Biden administration touts its economic record.

Antoni noted that major market moves such as this are typically driven by the “institutional investment class,” and that individual retail investors typically got crushed unless they had “incredible foresight.” Unless retail investors had an immediate need to sell, Antoni cautioned against doing so, urging retail investors to weather the panic.

“Now we’re faced with the reality of having to do it the hard way, of having to actually grow the economy and not just grow the money supply.” Antoni said.

Inflation was at 8.3% in August, significantly exceeding economists’ predictions with core prices jumping even higher, according to data from the Bureau of Labor Statistics’ Consumer Price Index (CPI).

Core prices, which measures all prices less food and energy, remained elevated at 6.3%, slightly higher than July’s 5.9%, according to the BLS. With core prices remaining strongly elevated, it is unlikely that the Federal Reserve will slow its rate of interest increases designed to combat inflation, and will once again hike rates by 0.75% next week, according to The Wall Street Journal. (RELATED: Fed Unveils Bleak Forecast In Another Troubling Sign For The Economy)

Economists had predicted inflation to decrease from 8.5% to around 8.1%.

“The Federal Reserve will require at least three months of reassuring inflation data—along with evidence of a cooling labor market—before considering softening its tone,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, according to the WSJ. This estimate is in line with the Federal Reserve’s estimate that the fight against inflation will likely take until the end of the year, according to a report.

The energy index continued to fall 5% from July, but energy costs have still increased 23.8% year-on-year, according to the BLS. Gasoline in particular remains high at 25.6%, down from 44.9% in July, with fuel oil remaining up 68.6% even after falling 5.9% in August.

Food prices posted the largest 12 month increase in 43 years, with a 11.4% year-on-year increase in national food prices, up from July’s 10.9%, according to the BLS. Prices for shelter also remain elevated, increasing 6.2% year-on-year, compared to 5.7% in July.

Under President Biden’s economic plan, we’re: – Bringing home jobs that went overseas – Making things here in America – Making our supply chains more secure – Winning the race for the future

The Biden administration has been taking a victory lap on economic conditions, with Treasury Secretary Janet Yellen claiming that the U.S. had undergone an exceptionally rapid recovery “by any traditional metric,” in remarks at a Ford electric vehicle facility Sept. 8. She went on to say that “Household balance sheets are strong.”

The Federal Reserve, which operates independently of the Biden administration, has been less optimistic, and described the economy as “generally weak” in a report just one day prior to Yellen’s speech. Roughly half of the regional banks that comprise the Federal Reserve system reported that their regional economies were either stagnant or declining, with the remainder reporting either slight or modest growth.

“Last month President Biden made a huge production over a 0.0% month-to-month change in the CPI from June to July,” said Peter C. Earle, economist at the American Institute for Economic Research in a statement to the Daily Caller News Foundation. “There isn’t anything to celebrate in today’s July-to-August CPI numbers, so the likely spin will be to return to touting the so-called Inflation Reduction Act.”

Know-nothing pundits and politicians have been communicating to Americans that inflation is, like the weather, a mystery they can’t control. That’s simply not true, write three economic commentators in a soon-published book, “Inflation: What It Is, Why It’s Bad, And How to Fix It.” On the contrary: inflation is a direct result of governments cheating their people, and solving it is pretty simple, if politically difficult.

In the book, businessman Steve Forbes, economist Nathan Lewis, and business journalist Elizabeth Ames give laypeople a concise, readable introduction to monetary policy. They also lay out easy-to-understand policy and personal prescriptions for responding to an inflationary economy such as today’s. The book is short and immensely useful for those of us who are not economic experts or finance minds and just want politicians to stop stealing our hard-earned money and endangering our nation’s security.

It would also be useful to members of Congress and other government officials with the authority to address what especially for the poorest Americans is a frightful economic situation. The authors lay out a one-year plan for stopping inflation in its tracks based on historical and international experience.

In the course of explaining what inflation is and how it works, the authors make the important point that it’s not just about money. Inflation is deeply connected to societal flourishing in general. Societies in which inflation is rampant are often unstable, chaotic, and violent.

“Markets are people,” the authors write. “When money is no longer a reliable unit of value, not only trade but social relationships ultimately unravel. Nations afflicted by extreme inflation end up experiencing higher levels of crime, corruption, and social unrest. As we have seen throughout history, the end result can be a tragic turn to strongmen and dictators.”

After electing a socialist president, Peru hit a 25+ year record inflation rate. The result? Citizens are now rioting over unaffordable food & gas prices.

Meanwhile, in the U.S., Democrat elites dismiss Americans’ concerns over 40+ year record inflation. https://t.co/X8YIHnsDc1

— María Elvira Salazar 🇺🇸 (@MaElviraSalazar) April 8, 2022

In an inflationary economy, the winners are the rich, the well-connected, and the corrupt. The losers are the poor, the middle-class, and those who work hard and play by the rules. Thus, an inflationary economy is inherently an unjust system. This is the top reason it should be combatted.

Not surprisingly, then, the rich and powerful often insist some inflation is a good thing. Maintaining a consistent level of inflation is in fact the Federal Reserve’s open policy goal. But even a “low” level of inflation such as The Fed’s (often wildly missed) target of 2 percent a year effectively steals significant income from especially the working and middle class. For someone earning $50,000 a year, 2 percent annual inflation is a $1,000 pay cut every year. That can be the difference between saving and not saving.

Making it harder to put money aside essentially forces middle and working-class people to depend on welfare rather than their own industry. Inflation thus erodes the middle class that is the bulwark of all free societies. So when it increases, societies tend to experience chaos. More people stop working and creating, and start trying to steal from others, either through government or through crime.

It should go without saying that an unstable society and economic chaos are threats to national security. These invite aggression from foreign enemies and hinders a nation’s ability to respond. This should make policymakers take inflation seriously, but like usual, so far politicians are mostly playing the blame game instead of solving the problem.

What Causes Inflation

Inflation is not merely rising prices, even sharply rising prices. That can occur for sensible reasons, such as sudden consumer demand for some fashionable item, or a crop failure leading to natural shortages. The authors define inflation instead as “the distortion of prices that occurs when money loses value.”

That can be seen, for example, in much of the current housing spike: “If you’ve made few, if any, home improvements and the local housing market isn’t on fire, you can be sure that the near-million-dollar sale price of your house doesn’t mean that it has magically become more valuable. Its worth has been distorted by a gradual, and totally artificial, decline in the value of the dollar,” explains “Inflation.”

When people stop trusting a currency as a stable measure of value, we get inflation. This is another way inflation is not solely about economics. It’s also about the people’s faith in their government and markets. That’s why lower-trust societies are more likely to experience inflation, and inflation is likely to worsen social trust. That’s also why inflation tends to spiral until somebody steps in to restore trust in the economy.

What causes inflation? If it’s true inflation, not price shifts caused by other market factors such as fads or innovation, it amounts to “a corruption of prices resulting from the debasement of currency by governments.” In other words, inflation happens when governments decide to circulate more money without a corresponding increase in economic value. This usually happens when governments want to spend more than they have, which is what the U.S. government has been doing for decades.

Today, the Federal Reserve essentially passes on federal debts and deficit spending to American consumers by creating more money without also creating new value. It is now one of many Western central banks that “effectively financ[es] their [government] deficits by buying their debt.”

In very simple terms, inflation is the result of governments spending far more than they can openly tax from citizens, then attempting to hide their shenanigans with financial gimmicks. So it is absolutely fair to think of inflation as a tax, and as the direct fault of shady government behavior: “Moderate inflation results from short-term ‘stimulus;’ hyperinflation comes from regular money printing to pay the government’s bills…The United States has not begun directly financing itself with large-scale money printing. Unfortunately, that may already be changing.”

Ending Inflation Is a Question of Political Will

The book helpfully explains in very clear and simple detail how the Federal Reserve enables Congress’s refusal to pay for its insane spending and how that all fuels inflation. It also discusses several intricate maneuvers by which this happens and why there isn’t a direct correlation in every case between money printing and inflationary effects. I won’t go into those here, but as a non-economist I did find them very helpful for understanding what’s going on.

I also found especially insightful the authors’ observation that federal overspending is not passed on to future generations, which is what I thought previously, but is inflated away from today’s workers and savers. Inflation is a tax on a nation that is unwilling to live within its means, and it occurs not in the future but in tandem with runaway government spending.

Ending inflation is quite simple, the authors say: “Stabilize the value of money.” Yet most “inflation remedies… more often than not end up making things worse.” That’s because government officials typically either misunderstand the root causes of inflation or are unwilling to take the steps necessary to address it. Thus, governments implement price controls or “austerity” measures, which usually further destroy their economies.

Instead, what’s needed is to tighten the money supply. The authors get into the details for doing this effectively, including their recommendation for the best way to ensure reliable money, a “new gold standard that would work in the twenty-first century.” They discuss this and respond to common arguments against it, still in highly readable prose.

Our Chief Obstacle to Fixing Inflation Is Ourselves

The key obstacle to implementing the authors’ one-year plan for restoring currency stability is widespread economic ignorance cultivated by leftist economists to preserve their control over policy. Yet given these economists have been wrong time and time again, it seems it’s high time to pay attention to experts whose recommendations have a reliable track record.

Unfortunately, since the majority of people working in Congress, the Federal Reserve, and similar commanding heights are the reason we’re in a dangerously inflationary economy in the first place, it’s probably too much to expect they will do anything other than make the situation worse in the near future. That’s why you’re hearing Joe Biden and other Democrats hint at making things worse with price controls or other punitive regulations by demonizing various industries for raising prices.

Not just because such people are at the helm, but also because they’ve already baked more money devaluation into the economic pie for the next several years, expect significant inflation to continue for quite some time. We can only hope and pray that the worst disasters of historic inflationary economies will be averted for us. And obtain some backyard chickens so we have something affordable to stick in the pot for dinner.

Joy Pullmann is executive editor of The Federalist, a happy wife, and the mother of six children. Sign up here to get early access to her next ebook, “101 Strategies For Living Well Amid Inflation.” Her bestselling ebook is “Classic Books for Young Children.” Mrs. Pullmann identifies as native American and gender natural. She is also the author of “The Education Invasion: How Common Core Fights Parents for Control of American Kids,” from Encounter Books. In 2013-14 she won a Robert Novak journalism fellowship for in-depth reporting on Common Core national education mandates. Joy is a grateful graduate of the Hillsdale College honors and journalism programs.

The San Francisco Federal Reserve published a study this week that appeared to contradict President Joe Biden’s narrative about inflation.

Americans are battling historic inflation and growing economic woes that appear to have no end in sight. In fact, the latest report from the Bureau of Labor Statistics showed the consumer price index has increased 7.9% over the past 12 months. Unfortunately, the buck does not stop with Biden. The president has blamed inflation and other economic problems on COVID-19, the supply chain, and even Russian President Vladimir Putin and the war in Ukraine.

The study sought to understand why U.S. inflation is increasing at a much higher rate than other advanced economic countries. The reason? The economists pointed toward COVID-19 relief bills, which pumped the economy, and Americans’ pockets, full of income. In fact, they argued the stimulus bills account for about 3% of inflation.

“Since the first half of 2021, U.S. inflation has increasingly outpaced inflation in other developed countries,” the study said.

“Estimates suggest that fiscal support measures designed to counteract the severity of the pandemic’s economic effect may have contributed to this divergence by raising inflation about 3 percentage points by the end of 2021,” the bankers explained.

This is Bidenflation. SF Fed chart literally shows the impact on inflation of Biden’s $1.9T 3/21 gov’t spending spree. It shows US inflation vs that in Canada, Denmark, Finland, France, Germany, Netherlands, Norway, Sweden, & the UK – the chart ends before Russia invaded Ukraine. pic.twitter.com/aEJyglsI0Q

Without the massive COVID relief bills, the economists suggested the U.S. could have experienced deflation, which has benefits and drawbacks. Still, they argued the impacts of deflation “would have been harder to manage,” a comment that should be taken with a grain of salt considering the government is having a difficult time managing the inflation crisis. Importantly, the study failed to conclude that Putin is to blame for inflation.

Because of inflation, Americans will spend approximately $5,200 more than last year, Bloomberg reported.

Inflation will mean the average U.S. household has to spend an extra $5,200 this year ($433 per month) compared to last year for the same consumption basket, according estimates by Bloomberg Economics. The excess savings built up over the pandemic, and increases in wages, will cushion those costs, and allow spending to expand at a decent pace this year. But accelerated depletion of savings will increase the urgency for those staying on the sidelines to join the labor force, and the resulting increase in labor supply will likely dampen wage growth.

According to a recent NBC poll, a “plurality of Americans” blame Biden and his policies for inflation, while they overwhelmingly reject Russia’s culpability for America’s economic woes, NBC News reported.

Treasury Secretary Janet Yellen acknowledged “rapid inflation” will persist for several more months after she repeatedly downplayed the risk of consumer price increases. Americans can expect consumer prices to continue their rapid rise until returning to normal in the “medium term,” Yellen said Thursday in an interview with CNBC. But Yellen, along with top Federal Reserve officials, predicted inflation wouldn’t be a concern.

“We will have several more months of rapid inflation,” Yellen told CNBC. “So I’m not saying that this is a one-month phenomenon.”

“But I think over the medium term, we’ll see inflation decline back toward normal levels,” she said. “But, of course, we have to keep a careful eye on it.”

Yet in February, Yellen downplayed the risks of inflation, saying the Treasury Department had the tools to deal with the risk “if it materializes.” She also pushed back on former Treasury Secretary Larry Summers’ warning that President Joe Biden’s $1.9 trillion coronavirus relief package would trigger massive, once-in-a-generation inflation.

Yellen added that the Biden administration was more worried about jobs than rising prices.

President Joe Biden speaks as Treasury Secretary Janet Yellen listens during a White House meeting on April 9. (Amr Alfiky/Pool/Getty Images)

One month later, the Treasury secretary downplayed inflation again when asked if the $1,400 stimulus checks included in the relief package could boost prices, according to the Associated Press. She again pushed the legislation, saying it was key for a full economic recovery.

“I really don’t think that is going to happen,” she said in the March 8 interview, the AP reported. “We had a 3.5% unemployment rate before the pandemic and there was no sign of inflation increasing.”

Then, one week later, Yellen doubled down, arguing again that there wouldn’t be significant inflation.

“Is there a risk of inflation? I think there’s a small risk and I think it’s manageable,” Yellen told ABC News.

“I don’t think it’s a significant risk,” she continued. “And if it materializes, we’ll certainly monitor for it but we have tools to address it.”

However, consumer prices have surged faster than they have in decades, according to government data. Economists also expect inflation to rise higher and for longer than previously expected.

In addition, several major U.S. corporations have recently announced price increases while the highest number of small businesses have reported price hikes since 1981.

These Leftist can’t even lie convincingly anymore, and it obviously doesn’t bother them. When they lie it’s their native language.

This article has been contributed by Dave Hodges and was published at The Common Sense Show.

What will happen first? Will we fall under the specter of martial law and all that entails? Or, will we experience an economic collapse prior to martial law?

In the present state of affairs, it is very easy to focus on the invasion of America through our Southern border as the Fifth column insurgents make their way into the country in the form of MS-13 as they prepare to wreak havoc on any opposition to the coming takeover.

We are also focused on the presence of unscreened immigrants coming into our country and who are failing to be screened for very serious health conditions such as Ebola.

It easy to become fixated on things like the NDAA and unconstitutional, permanent detention. We are very focused on the shoot down of MH-17 and preparing for war with Russia. However, what we should be focusing on is the economic collapse which has already began.

Before we continue with the analysis of what comes first, let’s interject some common sense into this analysis. The global elite need a horrific war to rid themselves of the old system and usher in the new system. Out of chaos comes order. This will set into motion the depopulation agenda that will accompany this coming martial law and World War III. We know the globalists seek to maximize profits at every turn. Therefore, one should ask themselves the question, “How can they globalists make the most money as they usher in the New World Order? The answer is simple, if they want to realize maximum value for their efforts, they should steal as much money from the American people as possible, before collapsing the economy.

Why An Economic Collapse Will Happen First

America only has to look at three economic indicators to know that we are in a lot of trouble, The budget deficit is $17 trillion dollars, unfunded (partially or otherwise) mandated social programs constitutes another $222 trillion dollars and the credit swap derivatives total between $1 quadrillion dollars to $1.5 quadrillion dollars. Based upon these numbers, America has clearly been set up to fail.

When we look at Social Security, Medicare, Medicaid and all the government programs that we all take for granted, the price tag is a whopping $222 trillion dollars. These numbers are going to be exacerbated and grow exponentially because the bulk of the baby boomers are entering retirement age. Even if we took every single penny that the federal government takes in and devote it to paying off these social programs, it would take 111 years to pay off this debt.

In the United States, credit swap derivatives created national debt totals of over one quadrillion dollars. That is one thousand trillion dollars! The entire GDP of the planet is estimated at $66 trillion dollars. And somehow, in the infinite wisdom of Congress in 2008, we falsely and naively believed that a $750 billion transfer of wealth (i.e., Bailout #1) was magically going to save the economy and the collective futures of the American middle class. In short, the debt created by futures speculation is approximately 16 times greater than the sum total of the entire wealth on the planet! And we think we are going to climb out of this? We could fund 1,000 bailouts and the eventual outcome will be the same, slavery by debt. We are being held in place, while our financial assets are being separated from our soon-to-be dead corpses.

The Collective Young Adult Work Force Has Little to No Future

The fruits of the labor of young adults has already been transferred to the elite.

In a part of the dead American Dream, we used to tell our children, “Study hard, go to college, get a degree and you will get a good paying job in your field. This former guidepost designed for preparing young people to successfully enter adulthood, should no longer be held up as an ideal. Please consider the following:

The number of Americans in the 16 to 29 year old age bracket with a job declined by 18 percent between 2000 and 2010.

Incomes for U.S. households led by someone between the ages of 25 and 34 have fallen by about 12 percent after you adjust for inflation since the year 2000.

Overall, approximately 25 million American adults are living with their parents according to Time Magazine. And this is because they cannot find decent work. President Obama tells us that our economy is on the rebound (after being robbed blind by the bail outs). However, the real unemployment statistics tells a far different story.

These real numbers tell the truth.

Where Did the Money Go?

When I was a third grader in Mrs. Strong’s third grade classroom, we conducted an experiment in which we had to determine how long it took for water to evaporate from a small glass. As we were in the process of watching the water evaporate from our glass, Mrs. Strong asked us where the water went? From this children’s science experiment, we learned that the water did not just go away, it went somewhere in real form and would return to us in the form of rainfall.

Look at the following chart below which measures price increases for basic essentials from January 2000 to March 2014. The numerical differences of what it costs to be an American in this economy is dramatic!

Where did the difference in the money go?

Where did the money go? Most people with their lack of knowledge of economics will look at this chart and answer “inflation” eats up our money. What our nation’s sheep is never taught is how to answer the question, what really causes inflation? In our schools, we teach the inflation is just a part of painful living, just like getting colds. Nothing could be further from the truth. It is contrived and its purpose is to control the people through debt slavery.

The first place to look for these price spikes is the Federal Reserve. Between the usury fees and interest they charge us for the “right” to use their money, our dollar is actually worth about 94 cents by the time we receive the dollar. The minion banks of the Federal Reserve pay you less than one percent to house your money, that they get to loan out. All things being equal, you losing about 5% per year in real buying power. This is a hidden tax that you pay to the elite which amounts to about 5% per year. As Mrs. Strong would say, the money did not just evaporate. It went somewhere.

What has chronicled above is what I label as indirect theft. Nobody is walking into your bank and stealing your money in these examples. Simply, financial practices and economic controls are created to slowly erode our wealth and transfer it to the elite. However, things are changing as we are transitioning from indirect theft to a very stark from of directly stealing the people’s assets by the elite.

Direct Public Theft of Private Assets

I have chronicled in a recent article that JP Morgan Chase and HSBC are making it almost impossible to wire money out of their banks into overseas accounts. This is the same as putting a bull’s eye on your money as they plan to seize as much as possible and they don’t want you to be able to control your money.

Over 50 percent of all stocks and bonds are owned by just 1 percent of the U.S. population. When the Stock Market crashed in 1929, who lost money? The elite already had their money parked on the sidelines when the crash came and when it did where did the money? That money went back into the hands of the people who created this Ponzi scheme. The same thing is about ready to happen again.

The elite are preparing for one last great garage sale. They are preparing to take every resource at your disposal.

Grand Theft America Prior to the Collapse: The Direct Transfer of Wealth

In no civilized country in the world do the banks have the right to steal money from citizen depositors. However, in America, this beta test was already being accomplished as ex-Goldman Sachs CEO and ex-senator and ex-governor, John “the Don” Corzine, stole 1.2 billion dollars from secured deposits from MF Global, lied to congress about his actions and today is enjoying the fruits of his thievery. Let’s not forget that the Seventh Circuit Court of Appeals who just ruled that banks can steal the money of its depositors and it is legal! This would have been a SHTF moment in every other Western country, but Americans are taking this grand theft on their backsides, sipping a beer and bemoaning the performance of their favorite NFL team. THE ELITE HAVE JUST ANNOUNCED THEIR INTENTION TO DIRECTLY STEAL YOUR WEALTH BY USING THE FORCE OF LAW.

Retirement Accounts Are First

Workers in modern nations have always had retirement as an incentive to work towards. Soon, the government will control all retirement accounts. Furthermore, if you live in America, you are not getting the best pension package compared to other Western nations as America ranks last in overall pension benefits. And this is in the backdrop of the Obama Administration, there are clear plans to seize your 401k pensions. This planned theft by the Obama Administration will prove to be a devastating blow to the American middle-class and will provide a knockout punch to any hope that the middle class clings to when it comes to transmitting wealth to their children and we are just a short time from realizing this inevitability. At least in Greece, the people rioted when the Goldman Sachs run government stole the people’s pensions to pay down the bankers part of the derivatives debt. Conversely, Americans are merely acquiescing and passively accepting the fact that Obama and his minions are planning to steal your bank accounts, your social security, your public pensions and your 401k accounts and the process has already begun with Treasury Secretary Lew as he is borrowing against select Federal retirement accounts. Obama has announced the “MYRA” (My Retirement Account; please see http://www.whitehouse.gov/blog/2014/02/11/myra-helping-millions-americans-save-retirement ). The theft of American home mortgages has been going on for some time. When one adds up the totality of what is happening, it is safe to say that retirement accounts will be made to fail.

The Globalist Playbook

The soon-to-fail retirement accounts is one liability that the elite will soon get to stop paying on, but not before they initiate another round of bailouts designed to save the retirement accounts from the conditions that they have created.