A Canadian pastor has “exiled” his family to Kenya after his government invoked emergency war measures to punish citizens who attended a protest where he prayed and sang the national anthem. Harold Ristau, a decorated veteran and seminary professor, participated in the “trucker convoy” against lockdowns last February, when The Federalist interviewed him last. He is now party to a lawsuit arguing the government’s response to Covid that included treating dissent as terrorism violated Canadians’ fundamental rights.

“The fight is far from over,” said Marty Moore, a lawyer for the Justice Centre for Constitutional Freedoms (JCCF), which is litigating Ristau’s case. More than 14 months after the protest, police arrested another convoy leader this May. Lockdown litigation will likely continue for several more years, Moore said. The same is true across the West.

For peaceably assembling to petition his government for one day last year, Ristau says, he was threatened with the removal of his security clearance and government confiscation of his retirement nest egg, kids’ college funds, and other life savings. Ristau says he’s also experienced serious damage to his reputation, career, and friendships after the government used anti-terrorism measures against peaceful protesters.

“There’s no protection, if a pandemic started tomorrow, from future mandates. So that’s why I was really open to coming here,” his wife, Elise Ristau, said, sitting beside her husband in a recent video interview from Kenya.

Besides dealing with overbearing health restrictions, their children were mocked at school for their family’s religious and political views, Elise Ristau told The Federalist. After enduring more than two years of severe social and government repression, the Ristaus moved outside Nairobi with their five children last August.

“I don’t know that I can go back and be a Christian in Canada. So that’s why we’re here in Kenya,” Harold Ristau said. There, the former chaplain with a Ph.D. in philosophy trains Kenyan pastors at the Lutheran School of Theology.

Confiscating Dissenters’ Life Savings

Government use of “debanking” to punish dissent is growing in the West. Prime Minister Justin Trudeau’s government used it on essentially every convoy participant authorities could identify, said Moore.

“As soon as they knew your name if you were on the ground [protesting] in Ottawa, they froze your bank account,” Moore told The Federalist. “…The federal government met with the banks, they gave the [protesters’] names to the banks, and the banks were then pushed to freeze the bank accounts of anyone with that name in their banks. It was a fascist collaboration.”

In May, American whistleblowers disclosed the FBI obtained, without any warrants, “a huge list” of citizens’ private banking data in its Jan. 6, 2021 capitol riot investigation. Investigators targeted any American who legally bought a firearm using a Bank of America account all the way back to the 1990s, the whistleblower testified.

Treating a Veteran Like a Terrorist

After the Canadian government announced it would freeze the bank accounts of convoy protesters and their mostly small-dollar donors without legal due process, rumors of bank runs spread. Multiple large Canadian banks appeared to shut down online operations soon after the announcement. Elise withdrew their family’s savings that Friday, too, she and Harold said. Like thousands of Canadians, they had donated to the convoy. Yet Ristau was the only one of the four plaintiffs in his lawsuit whose accounts were not frozen. He thinks it’s because of his military record.

“Some of the measures that were at least attempted to be invoked are the kind of measures you find to freeze terrorist financing,” Moore noted. “So peaceful protesters were the equivalent of terrorists and the government leaned on banks in the guise of a national emergency to freeze their bank accounts.”

Leftist activists also filed a class-action lawsuit against every Canadian who donated to the convoy. It seeks $300 million in damages. When before the convoy Canada experienced multiple race protests that included violence against stores and police, no class action was filed.

Christians Assisting Government Persecution

Canadian lockdowns kept gyms, restaurants, and liquor stores open but closed churches. Leftist protesters were allowed to yell and sing without masks, and the prime minister kneeled to them, all while provinces banned Christians from singing and chanting in church for years.

Rev. Johannes Nieminen wasn’t allowed to cross provincial borders to perform his pastoral duties, while other Canadians could do so for work, he told The Federalist. After he was denied border entry several times, he said, police finally let him through — but told him he wasn’t allowed to meet with parishioners or hold church services.

“If I’m going to go to the grocery store for physical food, I’m going to the church for spiritual food. If I’m going to the doctor’s office for physical medicine, I’m going to church for the medicine of immortality,” Nieminen said. His denomination believes Jesus Christ’s body and blood are physically present in the wine and bread of communion, and that Christians are commanded to physically eat these — impossible without gathering in person.

Until moving to pastor in New Mexico this summer, Nieminen was clergy in the same denomination as Ristau, the Lutheran Church Canada. He said lockdowns sharply divided many churches, and even though most Covid measures are now lifted, church leaders have largely failed to seek reconciliation and repentance, as commanded in the Bible.

“We need to repent. There’s been crazy division here, and we need to actually talk about it,” he said.

State-Run Western Churches

Nieminen said pastors who obeyed the government to treat churches worse than liquor stores and gyms taught lay people church is non-essential or can be conducted online. The Bible commands keeping a day of worship, meeting in person, singing hymns and psalms, and physically receiving the bread and wine of communion. Christians have done all these every week since the time of Christ.

Communion is a “sacrament,” an action God commands that produces faith and eternal salvation. Only pastors can deliver it, a tradition going back to Christ’s commissioning of His apostles. In all the great pandemics of history, priests and pastors knowingly braved death to bring the sacrament to the dying desperate for the peace and unity with God it promises.

Nieminen said he saw Canadian Christians publicly plead for the sacrament amid lockdowns that nearly lasted three years. They received no response from their pastors, who told Nieminen the pleading parishioners didn’t use the “proper channels.”

“There’s that lack of trust in pastors and a church that they see as giving up on them and basically persecuting them,” Nieminen said. “…They’re being coerced by tyrants to do something against their conscience, and then they go to church and then they’re hearing the same thing from the church.”

Within days of him praying at the protest, says Harold Ristau’s sworn affidavit, fellow clergy began refusing to let him preach and to take communion with him. Some checked with superiors on whether to commune him. Refusing communion to a church member is tantamount to excommunication.

Praying at the protest “demonstrated I was this political insurrectionist” to some clergy whose beliefs about Covid were shaped by state-funded, anti-Christian media, Harold Ristau said: “Prior to Covid, everyone recognized the media were a bunch of liars who hated Christians, but with Covid suddenly we trust them entirely.”

A Political Decision, Not a Health Decision

So far, “none of the [legal] challenges to worship restrictions on church services have succeeded” in Canada, said John Sikkema, a lawyer at the nonprofit firm ARPA Canada.

“Culturally, people find going to the gym very important and less so going to church,” Sikkema noted. “Especially when some churches don’t seem to care and don’t think it’s necessary.”

To secular authorities, keeping the economy going easily trumps the church’s work of caring for human souls, Sikkema noted. That’s why they opened restaurants while restricting churches despite similar health risks: “That’s not really a health decision, it’s a political decision about what’s important to the health of your society.”

Police regularly showed up at churches on Sunday mornings and fined pastors whose parking lots had too many cars, he said. ARPA Canada and JCCF litigated a number of those cases and were often able to get pastors’ fines negotiated down to charitable donations.

Most churches that capitulated to government discrimination against Christians were already declining before lockdowns, and disproportionate percentages of their members didn’t go back to church afterward. Churches that kept to historic orthodoxy, on the other hand, tend to have recovered better from post-lockdown membership losses and many have even grown, Nieminen and Sikkema noted.

Religious Freedom Better in Africa

The difficulty of raising their children in rapidly apostatizing Western culture also affected the Ristaus’ decision to move across the globe.

“Things are normal here, people have traditional values,” Elise Ristau said of Kenya. “It’s inconceivable to think of transgender mutilation. As a mother and father, we do our very best to keep our kids Christian.”

In Canada, Christians are often required to lie or betray their faith to access government grants and licensing credentials, and avoid punishment in many professions, Sikkema said. Many Canadian doctors, lawyers, and teachers, for example, are required to endorse abortion and LGBT sexual acts.Canadian doctors and many other health care workers must help patients obtain an abortion or doctor-assisted suicide.

In 2018, Canada’s Supreme Court banned a Christian law school from opening over Christian sexual standards. The Canadian military is also working to eject chaplains over Christian sexual ethics. Just about every Canadian business sports a government-provided pride flag, Nieminen said. Churches that object to transgender mutilation of children have faced naked protesters as families arrive to worship, Sikkema said.

“Canadians are very aware that we don’t have freedom of religion, we don’t have freedom of speech, we don’t have the right to assemble if that’s in disagreement with the regime,” Nieminen said. “Pastors and teachers cannot speak about the morality of human sexuality. That is a reality Canadians live in, and I think that’s partly why they’re afraid to speak out.”

Christians Welcome in Kenya

The Ristaus had been invited to their current post before lockdowns, but Elise hadn’t wanted to uproot after moving the family so many times for Harold’s military career. They had bought land in Canada for their dream home and planted more than 1,000 trees on it.

“I had dreamed of this perfect life for myself in Canada,” Elise said. But then “there was a kind of turning point where I said, ‘We can go. Nothing is holding us here.’ It was a ‘shake the dust off our boots’ moment.”

From Toronto to Nairobi is approximately 7,500 miles. Flying commercially between the two takes 16 hours or more.

“In Kenya, I know it’s poor, and there’s corruption, but we’re not getting arrested for praying silently outside abortion clinics,” Elise said. “For a Christian in Canada, it’s pretty bleak.”

Joy Pullmann is executive editor of The Federalist, a happy wife, and the mother of six children. Her latest ebook is “101 Strategies For Living Well Amid Inflation.” Her bestselling ebook is “Classic Books for Young Children.” An 18-year education and politics reporter, Joy has testified before nearly two dozen legislatures on education policy and appeared on major media from Fox News to Ben Shapiro to Dennis Prager. Joy is a grateful graduate of the Hillsdale College honors and journalism programs who identifies as native American and gender natural. Her several books include “The Education Invasion: How Common Core Fights Parents for Control of American Kids,” from Encounter Books.

The House Oversight Committee issued subpoenas to banks asking for the Biden family’s financial records.

Fox News has confirmed that the Oversight Committee subpoenaed Bank of America, Cathay Bank, JPMorgan Chase, HSBC USA N.A., as well as former Hunter Biden business associate Mervyn Yan asking for financial records.

Rep. Jamie Raskin, D-Md., the top Democrat on the Oversight Committee, complained that Committee Chairman James Comer, R-Ky., was trying to hide information regarding the investigation from Democrats on the committee.

House Committee on Oversight and Accountability Chairman James Comer, R-Ky., leads an organizational meeting for the 118th Congress, at the Capitol in Washington, Tuesday, Jan. 31, 2023. (AP Photo/J. Scott Applewhite)

In a statement to Fox News, Comer said “Ranking Member Raskin has again disclosed Committee’s subpoenas in a cheap attempt to thwart cooperation from other witnesses. Given his antics with the first bank subpoena, the American people and media should be asking what information Ranking Member Raskin is trying to hide this time. No one should be fooled by Ranking Member Raskin’s games. We have the bank records, and the facts are not good for the Biden family.“

President Joe Biden and his son, Hunter Biden, step off Air Force One, Saturday, Feb. 4, 2023, at Hancock Field Air National Guard Base in Syracuse, N.Y. (AP Photo/Patrick Semansky)

The Oversight Committee Democratic staff sent a memo to members on Thursday which accuses Republicans of conducting their investigation behind a “veil of secrecy.”

“Despite this massive investment of time and resources, Republican efforts on this and other congressional committees have failed to yield any evidence of misconduct by President Biden. Nevertheless, Chairman Comer has issued six document subpoenas for financial records as part of this renewed investigation, several of which have been based on information Committee Republicans know to be false,” the memo states.

The Democratic memo alleges that Republicans haven’t been publicizing their subpoenas or notifying Democrats, which has purportedly resulted in some targets of subpoenas being unaware that the committee is seeking their records.

President Biden speaks during the annual House Democrats Issues Conference at the Hyatt Regency Hotel in Baltimore on March 1, 2023. (Drew Angerer/Getty Images)

“On February 27, 2023, Chairman Comer secretly issued the Committee’s first document subpoena as part of Committee Republicans’ ongoing investigation into the Biden family to Bank of America. This subpoena sought, among other information, “all financial records” from January 20, 2009, to the present — a staggering 14-year period — for John R. Walker, a private U.S. citizen… Yet, because of Chairman Comer’s use of a secret subpoena, Mr. Walker was never notified that the Committee had subpoenaed his financial records from Bank of America, he was never notified that Bank of America turned over his records to the Committee, and he was never notified that the Committee was publicly releasing information from these records,” the memo states.

Chad Pergram currently serves as a senior congressional correspondent for FOX News Channel (FNC). He joined the network in September 2007 and is based out of Washington, D.C.

It’s painful for me to watch so many smart pundits and politicians on both the right and the left buy into a media narrative that seeks to blame “wealthy speculators” or “tech bros” or venture capitalists for a banking crisis that ultimately started in Washington. Let me explain.

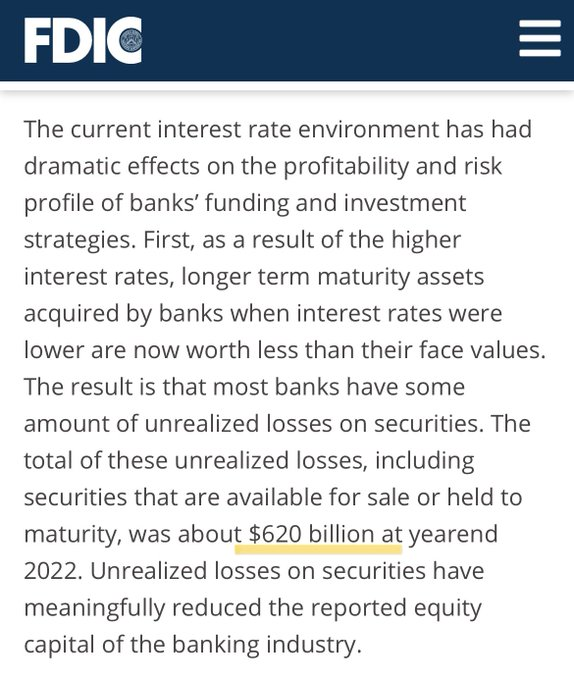

If you want to understand the context for the crisis, look at the Federal Deposit Insurance Corporation chair’s March 6 testimony — a week before Silicon Valley Bank’s collapse — where he explains that banks were sitting on $620 billion of unrealized losses from long-dated bonds. This provided the tinder for the crisis.

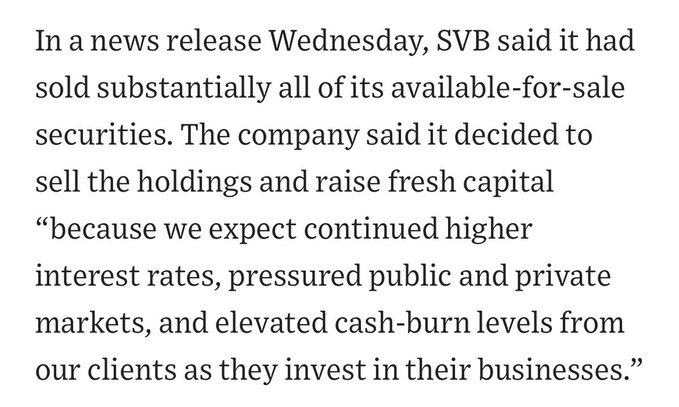

The match was lit when SVB announced on Wednesday, March 9, that it had effectively sold all of its available-for-sale securities and needed to raise fresh capital because of large unrealized losses from its mortgage bond portfolio.

Screenshot: Wall Street Journal

On Thursday morning, the financial press widely reported SVB’s need for new capital, and short sellers were all over the stock. The CEO’s disastrous “don’t panic” call later that morning only heightened fears and undermined confidence in the bank.

The idea that one needed “non-public information” to understand that SVB was at risk is drivel being peddled by populist demagogues. Any depositor who could read The Wall Street Journal or watch the stock ticker could understand there was no upside in waiting to see what would happen next.

By Friday, the run on other banks had begun. This became abundantly clear when regulators placed Signature Bank in receivership, announced a backstop facility for First Republic, and temporarily halted trading of regional bank stocks on Monday. Even trading of Schwab was halted.

Some unscrupulous reporters and political types have even claimed that I somehow caused this through my tweeting. Dang, they must think I’m Superman! Or maybe E.F. Hutton. But the timing doesn’t line up at all, as I already explained.

In the never-ending quest for scapegoats, some reporters and political types are asking if @theallinpod could have influenced the bank run. We didn't publish until Saturday morning when banks were already closed! I also never tweeted about SVB until it was already in receivership…

Once the run on the bank started, decisive action by the Fed was imperative. This meant protecting deposits (uninsured are 50 percent) and backstopping regional banks. No matter how distasteful you may find those things to be, preventing a greater economic calamity was necessary.

But back to SVB: Its collapse was first and foremost a result of its own poor risk management and communications. It should have hedged its interest rate risk. And it should have raised the necessary capital months ago through an offering that didn’t spook the street.

SVB doesn’t deserve a bailout and isn’t getting one. SVB’s stockholders, bondholders, and stock options are getting wiped out. The executives will spend years in litigation and may have stock sales clawed back. Anyone who thinks there’s a “moral hazard” isn’t paying attention.

But it’s important to understand that SVB’s failure didn’t arise from risky startups doing risky startup things. It arose from SVB’s over-exposure to boring old mortgage bonds, which were considered safe at the time SVB bought them. Perhaps this is why SVB had an “A” rating from Moody’s and had passed all of its regulatory exams.

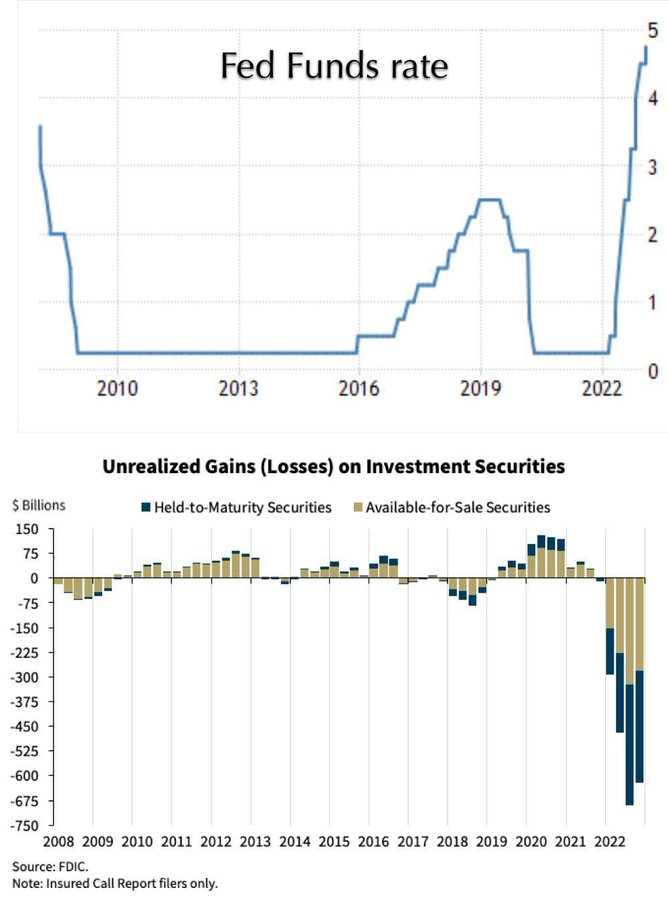

What turned the mortgage bonds toxic? The most rapid rate-tightening cycle we’ve seen in decades. You can see the connection here between rapid rate hikes and unrealized losses in the banking system.

So, what caused the rapid rate hikes? The worst inflation in 40 years. And what caused that? Profligate spending and money printing coming out of Washington — all while Joe Biden, Janet Yellen, and Jerome Powell assured us inflation was “transitory.”

I warned two years ago that pumping trillions of dollars of stimulus into an already hot economy was an unprecedented and likely dangerous experiment. But this was Bidenomics.

Bidenomics = pumping trillions of dollars of stimulus into a rip-roaring economy. I’m not going to pretend like I know what’s going to happen next. AFAIK we’ve never tried this before.

So, when Joe Biden says he’s going to hold those responsible for this mess fully accountable, he ought to start by looking in the mirror. But I’m sure that’s not going to happen, just as I’m sure the hunt for scapegoats is just beginning.

David Sacks is an entrepreneur and author who specializes in digital technology firms. He is a co-founder and general partner of the venture capital fund Craft Ventures and was the founding COO of PayPal.

Last week, Canadian Prime Minister Justin Trudeau announced the suspension of Canadians’ rights last week in his invocation of the Emergencies Act to stop the Freedom Convoy protests in Ottawa and elsewhere. Among the restrictions announced are greater controls over the online crowdfunding sites that help to fund the protesters and attempts to control the flow of cryptocurrencies like Bitcoin. According to news reports, “credit card processors and fund-raising services will be required to report any blockade-related campaigns to Canada’s anti-money laundering agency.” Canadian banks quickly fell in line with the decrees, with Toronto-Dominion Bank freezing two personal bank accounts containing C$1.4 million ($1.1 million) they said was intended to support the truckers.

It bears a striking resemblance to the Biden administration’s recent efforts to intensely monitor what goes in and out of Americans’ bank accounts. The president’s expected announcement this week of an executive order to explore greater regulation of cryptocurrency is likewise an attempt to stick the state’s nose ever deeper into the average citizen’s business.

You Don’t Control Your Money Like You Used To

We’ve grown used to the idea that the government has a monopoly on money. Coining money is one of those powers of the state that most people never consider, like building roads or controlling national borders. Our money has dead presidents on it — it’s plainly a government operation. Where else would money come from, right?

But before the rise of electronic money transfers — the electronic bill-pay, direct deposit, and credit and debit card purchases we make every day now — whether the dollar bill in your wallet was issued by a bank (as in the early days of the republic) or by the Federal Reserve (as they are now) did not much matter. It was yours. No one knew what you spent it on unless you chose to tell them. That meant greater privacy, both from your neighbors and from your government. But it also entailed risk. Cash could be stolen, lost, or destroyed, and there was no way to get it back. And it was cumbersome, especially as inflation ate away at the value of a dollar. Could you bring cash for a down payment on a house? Sure. It still happens. But hauling a suitcase full of cash invites the scrutiny of thieves and the state — even when it’s completely legal.

The convenience of electronic money has been clear for decades now, but the dark side is showing itself this year like never before. All of the convenience of moving money around effortlessly comes at the cost of losing control over it.

How Goverment Uses Control of Your Money to Control You

These digital transfers feel, to most of us, like magic. A volley of ones and zeros flies through the cybernetic ether and — poof! — your electric bill is paid. But in truth, the data is routed through banks, and there are fewer of them all the time. Those remaining, many-times-merged financial giants that handle our affairs are, for all their clout and power, susceptible to government pressure.

We have seen it already when the Obama administration leaned on banks to refuse to deal with people involved in marijuana or the sex trade, even where those businesses were legal at the local level. No federal law gave them this power: the threat was enough. And where people keep money in cash, the government often finds a way to take it without even bothering to charge the owners with a crime.

Trudeau’s emergency measures take advantage of these pressure points and lean on banks to choke off the complete flow of money to and from those he deems enemies of the state. No charges, no trial, just shutting it down. Now Trudeau’s government wants to make these “temporary” measures permanent. The slippery slope is usually not so steep, but these are strange times.

Governments have always used the word “emergency” to do what they want and to trample the liberties of the dissenting minority. Control over our money makes that easier than ever. Even the more self-sufficient among us engage in trade and unless you choose to live like a hermit, money is a part of that.

How Crypto Challenges the Government Monopoly on Money

Governments understand that alternatives to state-issued money, like cryptocurrency, are a threat to that hegemony. Trudeau and Biden demonstrate that in their recent efforts to control Bitcoin and other cryptocurrencies. But the beauty of these new systems is that they are made, purposely, to be beyond the control of any person or government.

When Bitcoin launched more than a decade ago, most of us (myself included) barely understood what it was or how it worked. Fake money for dark web mischief, I figured, an eventual failure at best, a scam at worst. Yet here we are in 2022, where government-issued money is eroded by inflation and controlled by statist decrees. They leave peaceful opponents with a choice between the old (gold) or the new (crypto). And crypto is a heck of a lot easier to carry around.

In deciding an earlier banking law question in McCulloch v. Maryland in 1819, Chief Justice John Marshall said that “the power to tax involves the power to destroy.” Two centuries on, we could apply a modern twist: the power to regulate involves the power to control.

Cryptocurrency was just a passing fad until government overreach made it a necessity. Decades of deficit spending have inflated the currency and decades of creeping statism have given the government massive power over how money is used. The government’s monopoly on money has failed and, like it or not, cryptocurrency is at least part of the answer.

Kyle Sammin is a senior contributor to The Federalist, the senior editor of the Philadelphia Weekly, and the co-host of the Conservative Minds podcast podcast. Follow him on Twitter at @KyleSammin.

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

NEWSMAX

News, Opinion, Interviews, Research and discussion

Opinion

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

You Version

Bible Translations, Devotional Tools and Plans, BLOG, free mobile application; notes and more

Political

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

NEWSMAX

News, Opinion, Interviews, Research and discussion

Spiritual

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

Bible Gateway

The Bible Gateway is a tool for reading and researching scripture online — all in the language or translation of your choice! It provides advanced searching capabilities, which allow readers to find and compare particular passages in scripture based on

You must be logged in to post a comment.