A number of headlines have been making the rounds declaring that Black Lives Matter is going bankrupt. These are misleading, not only because they conflate the Black Lives Matter Global Network (BLM GN) and the BLM movement, but also because BLM GN is not, in fact, on the verge of bankruptcy. To a certain extent, the confusion is understandable. BLM GN is the most visible and well-known of the various BLM organizations, the one founded by movement figureheads Patrisse Cullors, Alicia Garza, and Opal “Ayo” Tometi. When the general public hears “BLM,” this is who they think of. The BLM movement is not known for its transparency, and it’s easy to confuse its various members and their alphabet soup of acronyms.

While BLM GN fancies itself as the head of the BLM movement, the reality is that BLM is a many-headed hydra. BLM GN ostensibly was once the parent organization of a multitude of grassroots BLM chapters, but disputes over funding and priorities have led many of them to part ways with the organization, some becoming entirely independent entities and others banding together to form new collectives (for example, the “BLM 10+”). Most of the BLM movement’s heavy lifting is done by these grassroots chapters.

Then there is the Movement for Black Lives (M4BL), a shadowy collective of more than 150 activist organizations that is even more radical than BLM GN. M4BL provides funding and administrative support to its members and is currently a fiscally sponsored project of the Common Counsel Foundation (in 2020, it was fiscally sponsored by the Alliance for Global Justice [AfGJ], a Marxist revolutionary front with ties to the Sandinistas).

The group refuses to disclose the bulk of its members, but among those that it does disclose are Southerners on New Ground, Black Alliance for Just Immigration, UndocuBlack Network, Black Feminist Future, Organization for Black Struggle, Ella Baker Center for Human Rights, BlackOUT Collective, Highlander Research and Education Center, and the Black Movement Law Project. It received more than $30 million in donations in 2020, and that figure doesn’t include contributions made directly to its members. Why the group hasn’t received more media attention is a mystery.

Lastly, there is the BLM movement’s vast NGO archipelago, a menagerie of subversive organizations working tirelessly to advance the movement’s revolutionary agenda. These organizations include BLM GN’s official partners such as the NAACP and wholly independent outfits such as BLM At School, which with the help of the National Education Association (NEA) reaches children in thousands of schools across the country.

Even if BLM GN were to go bankrupt, these other organizations — the heart of the BLM movement — would live on. But reports that BLM GN is insolvent or going bankrupt are false. A cursory examination of BLM GN’s Form 990s shows that in 2020-2021, it raked in nearly $80 million in grants and donations, but the following year, that number fell to just over $9 million. Meanwhile, the nonprofit spent a little over $17 million and saw its investments drop by nearly $1 million. This meant it ended the year $8.5 million in the red.

That is where many journalists stopped reading. But a closer look reveals that BLM GN retains more than $40 million in its coffers from its record 2020 haul. Because it is a grantmaking organization helmed by a skeleton crew, it can easily pare back its spending over the coming year to balance its books.

That’s not to say that BLM GN has acted in a fiscally responsible manner. Its penchant for luxury real estate is well known, as is its proclivity for self-dealing. The nonprofit spent $6 million on a sprawling mansion in Los Angeles and granted M4BJ, a subgroup of BLM Canada, $8 million which was subsequently spent on a 10,000-square-foot Toronto mansion formerly owned by the Canadian Communist Party. Patrisse Cullors and her spouse, BLM Canada and M4BJ co-founder Janaya Khan, have purchased at least four high-end houses for $3.2 million in the U.S. alone. Interestingly, BLM Canada is one of the few regional BLM chapters to have actually received funding from BLM GN.

Meanwhile, BLM GN continued to hire relatives of Cullors and its board members. According to the organization’s tax filings, Paul Cullors, the brother of Patrisse Cullors, founded two private security companies which were paid $1.6 million in 2022. He was also paid a $126,000 salary as “head of security” despite being a graffiti artist with no experience in security. The previous year, BLM GN paid $970,000 to a company owned by Damon Turner, the father of Cullors’ child.

That same year, Shalomyah Bowers, who replaced Patrisse Cullors at the helm of BLM GN after her resignation, paid his own consulting firm $1.7 million. And $1.1 million was paid to New Impact Partners, a firm owned by Danielle Edwards, the sister of former BLM GN board member Raymond Howard. BLM GN also agreed to pay $600,000 to an unidentified former board member’s consulting firm in connection with a “contract dispute.”

Given the amount of money remaining in BLM GN’s coffers, it’s likely that the nonprofit will continue to behave in accordance with its current modus operandi. But again, this reprehensible organization is just one member of the greater BLM movement, which features a host of more serious actors that don’t squander their resources. BLM’s opponents would be wise to remain vigilant and refrain from declaring victory prematurely.

John Cohen is an Investigative Fellow at the Claremont Institute’s Center for the American Way of Life. He holds a B.A. in Molecular Biology and Public Health from Hampshire College and a M.A in Security Studies from Georgetown University’s Walsh School of Foreign Service.

The contrast couldn’t be clearer. A devastating train derailment and subsequent toxic fires rock a community in Ohio that President Trump carried by 29 points. Forty days later, President Joe Biden has yet to set foot in East Palestine despite numerous pleas from residents.

A few weeks after the train crash, news breaks about a well-connected bank few have ever heard of crumbling on a Friday afternoon. At a time of the day his supporters say he usually does nothing, Biden is in front of the television cameras telling the world that the U.S. government will bail out Silicon Valley Bank, which is located in a city Biden won by almost 50 points. Biden’s climate buddies and Gov. Gavin Newsom’s wine companies are no doubt relieved.

For those keeping score: Silicon Valley Bank (SVB) is an emergency that requires Biden to get out of bed before 9 a.m., while the people of East Palestine continue to wait for answers.

Looking at those who work with or benefit from SVB, one begins to understand Biden’s urgency. The White House may say climate is our worst existential crisis, but it looks like green dollars for leftists’ eco-friends required the quickest action.

It’s easy to wonder if President Biden’s actions are driven by the bank’s connection to climate companies. This article highlights a few, noting “Silicon Valley Bank served as a banker to dozens of climate and energy-tech companies, holding their cash on a day-to-day basis and issuing billions of dollars in loans in support of the type of large-scale, one-off projects that are essential to the sector.”

Read it again: Dozens of climate companies. Billions in loans. Holding their cash on a day-to-day basis. Now, it gets interesting.

Steyer once played a key role on a Zoom fundraiser for Biden that raised $4 million dollars. That’s a lot of money for a single conference call. Many of the donors were from Silicon Valley and have deep pockets. That’s why it should be no surprise that when it came time to find someone to oversee $369 billion in taxpayer dollars for green investments, Biden would reach back into Steyer’s world.

Another company reported to have close ties to SVB is Lowercarbon Capital. It doesn’t take long on their website to find their managing partner is a strong Biden ally. They proudly tell you the partner is not only a longtime supporter of President Biden and Vice President Kamala Harris, but “was on their 2020 campaign’s National Finance Committee and is a member of Climate Leaders for Biden.”

Wait, there’s more. According to the reports, another major company with ties to SVB is Sunrun Solar. The company saw money from SVB going back to 2014 and arranged for a loan of more than half a billion dollars less than three months ago.

All this government cheese would be bland without a little wine. Take a moment to appreciate Newsom’s tone-deaf actions about SVB. Not long after Biden’s announcement, Newsom heaped praise on the move, and now we’re starting to see why.

Newsom is the owner of some wine companies, and you’ll be shocked to hear those companies are reportedly held by SVB. And if you can handle one more vomit-inducing dose of hypocrisy, an SVB bank president sits on the board of a charity run by Newsom’s wife.

Joe Biden’s Climate Cult: Membership has its privileges. It’s too bad the people of East Palestine couldn’t get in on the ground level.

Larry Behrens is the Communications Director for Power The Future and has appeared on Fox News, Newsmax and One America News. You can find him on Twitter at @larrybehrens or email at larry@powerthefuture.com.

Arecession is coming in 2023, concluded more than two-thirds of the economists at big financial institutions recently surveyed by The Wall Street Journal. Inflation is also likely to remain high. Measuring year-over-year inflation by the U.S. government’s 1980s methodology put it at 15.23 percent in November 2022 instead of the government’s claimed 7.11 percent, according to economist John Williams.

Many commentators, including me, were wrong when we previously claimed our grandkids will be paying off America’s massively unaffordable welfare state. We are all paying for it right now and are likely to be for much of our lives in inflation and other economic devastation.

Nobel Prize-winning economist Milton Friedman’s maxim that “inflation is always and everywhere a monetary phenomenon” — meaning, inflation is always caused by government overspending — predicts continued inflation for at least the next five years, if not longer.

That’s because government entities are continuing to engage in seriously inflationary actions. They’re doing this partly because of ideology, partly to buy votes, and partly because they prefer eating away Americans’ savings to paying off the unprecedented government debt that politicians have accumulated in the last 70 years enriching their friends and buying off voters.

Inflation Means Politicians Stealing from You

A 2021 Politico profile of a former U.S. Federal Reserve member noted, “Between 2008 and 2014, the Federal Reserve printed more than $3.5 trillion in new bills. To put that in perspective, it’s roughly triple the amount of money that the Fed created in its first 95 years of existence. Three centuries’ worth of growth in the money supply was crammed into a few short years.”

That dissenting former Federal Reserve committee member, Thomas Hoenig, “was worried primarily that the Fed was taking a risky path that would deepen income inequality, stoke dangerous asset bubbles and enrich the biggest banks over everyone else,” the profile says. “He also warned that it would suck the Fed into a money-printing quagmire that the central bank would not be able to escape without destabilizing the entire financial system.”

Essentially, the Federal Reserve has been helping Congress manufacture money to buy up the public debt they contracted by promising Americans more stuff than we can pay for. That’s been ongoing since the 1960s Great Society, which basically paid Americans with unaffordable entitlements to shut up about the steady loss of their constitutional freedoms, according to scholar Christopher Caldwell.

The Borrowing Will Go On Until It Can’t

In 2021, 41 percent of federal spendingdependedon borrowing. In 2022, 22 percent did. This means raising the cost of debt by hiking interest rates, as the Fed is now doing, could provoke a crisis because it would make Congress’s unsustainable behavior even more painful.

As a Manhattan Institute analysis by economist Brian Riedl notes, “rising interest rates risk pushing government interest costs, annual budget deficits, and total government debt to unsustainable levels … once the debt surges, even modest interest-rate movements can impose stratospheric costs.”

This would call years of government bluffing about the state of federal finances and institutions. It would require Congress not only to stop spending but to cut programs, which means angering voters. It would usher in the unavoidable and painful new era of managing America’s decline.

“Once a debt-and-interest-rate spiral begins, it is nearly impossible to escape without drastic inflation or fiscal consolidation,” Riedl notes.

However this ends, it is likely to include a lot of economic pain, one way or another. Here are just a few of the many indicators that inflationary times are not going away fast.

1. ‘Covid’ Overspending Continues Until at Least 2024

The funds for the sixth waste-packed “Covid relief bill” will be distributed to big-government donors, states, and local governments through the end of presidential election year 2024. Yes, the American Rescue Plan Act from Covid-tide sends states and local governments $350 billion that is still being rolled out — by design.

That law’s total spending comprises more than 100 times states’ 2020 budget shortfalls, and many state and local governments can hardly figure out what to do with all the money. As they take years to spend it, that money will keep juicing inflationary pressure. A similar effect is occurring with all the so-called Covid relief bills, which together sent $6 trillion spinning through the economy, devaluing our currency. Much of this wild inflationary deficit spending has been electronically printed through the Federal Reserve.

Together, 2020s federal spending allegedly in response to Covid was more than double the inflation-adjusted federal response to the 1930s Great Depression. We’re already seeing the inflationary effects of all this so-called Covid spending, and it’s not over yet.

2. Democrats and Republicans Recently Went on Even More Inflationary Spending Binges

In conjunction with Democrats’ mega-spending “infrastructure” and “green energy” bills soon after Covid that also helped them win Congress and the presidency in 2020, all this extra spending is projected to increase the federal debt by an unprecedented $6.5 trillion, costing more than the 20 years of U.S. occupation of Iraq and Afghanistan, according to Riedl.

“In other words, the U.S. government is in the early stages of what is projected to be the largest government debt binge in world history,” Riedl notes.

That doesn’t even include the massive federal spending expansions to support a large army of grifters profiting off the human suffering of the Russia-Ukraine war in 2022. Congress spent more on the first four months of Ukraine’s war than it did on the first five years of its undeclared war in Afghanistan.

Atop all this, more deficit spending is likely to come. In August 2022, Democrats confirmed yet again that historic levels of inflation that year were no impediment to their big-spending aims when Biden announced that he’d force taxpayers to assume up to nearly $1 trillion in student loans taken on by largely higher-income professionals. That spending is tied up in court and could be allowed at any time.

This all means that the source of inflation — government overspending — is at an unprecedented rate and pace, and even with the House Freedom Caucus’ negotiated limits on congressional spending activity, trillions in new spending is already locked in.

3. Build Back Bankrupt Shoveled Yet More Out the Door for Years to Come

In 2022, the Biden administration managed to get its top-priority grab-bag of increased government spending signed into law. By spending more money the government does not have and imposing more taxes, the ridiculously named Inflation Reduction Act is likely to increase inflation, said a Tax Foundation analysis.

“By increasing spending, the bill worsens inflation, especially in the first four years, as revenue raisers take time to ramp up and the deficit increases,” the foundation’s analysis says. “We find that budget deficits would increase from 2023 to 2026, potentially worsening inflation.”

Continuing to shovel money to cronies while ignoring major structural problems in the U.S. economy and federal budget process has become a hallmark of Congress in the 2000s. This has to end at some point, but until that point comes reasonable people can only expect such legislation to continue to pass, and to continue to worsen inflationary pressures.

Given how reckless both parties have been for decades on fiscal matters, it is likely this norm of spending money Congress can’t actually appropriate will continue until a major disaster ends their ability to fake.

4. Federal Officials Are Destroying the People’s Trust

Inflation happens “When money is no longer a trustworthy measure of value,” note Steve Forbes, Nathan Lewis, and Elizabeth Ames in their 2022 book, “Inflation.” Inflation is at least partly about a crisis of confidence in government — a warranted one, usually, because major inflation occurs as a result of politician malfeasance. Unfortunately, U.S. government officials are doing nothing to restore the people’s lost confidence in them — in fact, just the opposite.

In 2022, federal officials spent months denying inflation was happening. They also denied the United States was in a recession, insisting the traditional definition of two economic quarters in contraction was false when it was applied under Democrat rule. They’ve switched how they measure inflation to hide a large part of it.

U.S. leaders also refuse to stabilize our currency, instead taking actions that further erode Americans’ ability to put food on the table and get ahead through legitimately productive honest labor (as opposed to bullsh-t jobs). This does the opposite of what is needed: restore confidence in our markets by announcing strong steps to strengthen the U.S. dollar. They are also engaging in other activities that only erode confidence in the U.S. financial system, such as monetizing the federal debt and refusing to stop massive deficit spending.

Because politicians have created this situation and keep refusing to actually address it, Americans increasingly don’t trust their government or our debt-driven financial system. Polling shows public trust repeatedly hitting new record lows for every social and political institution. That’s an economic problem as well as a political and cultural problem, because a lack of confidence in markets can trigger economic growth, recession, and panics.

Usually, such crises build under the surface for a long time and then burst out into the open all of a sudden. As Hoover Institution economist John Cochrane said during a panel discussion, “Debt crises are like the Spanish Inquisition; no one expects them to come. If you knew they were coming, they would have already happened.”

5. The U.S. Federal Government Is Effectively Bankrupt and Inflation Helps It Hide That

The on-books U.S. national debt of $31.5 trillion is just the tip of the iceberg. Our entitlement systems are about to start going bankrupt, adding trillions in additional financial burdens on taxpayers. Riedl notes, “The U.S. government is projected to run a staggering $112 trillion in budget deficits over the next three decades, driven mostly by Social Security and Medicare commitments that are already set in law.”

If one adds unfunded and other liabilities that government officials keep off the books such as Federal Reserve debt, the amount the U.S. national government owes is more than $200 trillion. That doesn’t include what state and local governments owe, and many of them are also bankrupt or getting there.

“No matter what interest rate you use, the U.S. needs to immediately and permanently raise every federal tax by at least one third to pay, through time, for what our government plans to spend,” Boston University economist Laurence Kotlikoff wrote with fellow economist John Goodman in 2021. “The alternative? Massive spending cuts. And, no, the Federal Reserve can’t make this problem go away by printing the money needed by the Treasury. This would end where it always does — in hyperinflation.”

U.S. debt, deficits, and unfunded liabilities — which together form a total picture of U.S. national economic entrapment — are the largest ever measured in world history. Besides Japan, which isn’t spending the majority of its debt on entitlements like the United States is, “Greece and Italy are the only other OECD countries with a total government debt exceeding that of the United States,” Riedl notes. Greece and Italy have had major sovereign debt crises that have destroyed their standards of living and brought their economies into long-term decline.

“When you look at these numbers, you realize we’re Argentina in 1910,” Kotlikoff told CNBC in 2018, before the alarmist Covid response and Biden presidency made things much worse. All it will take for these scary structural problems to become visible and impossible to ignore is a financial panic or another major event like a war. Oh, look, Congress is also pushing us ever-toward open war with Russia instead of toward peace. Brilliant.

6. Child Scarcity Will Drive Higher Prices

In March 2022, The Wall Street Journal reported the opinion of retired British central banker Charles Goodhart that global structural factors will drive higher inflation for years to come. Goodhart helped Prime Minister Margaret Thatcher break inflation in the 1980s. He told the Journal that the rising global crisis of child scarcity will also push inflation up for decades.

As labor becomes more scarce, he maintained, workers will push for higher wages, in turn driving up prices. At the same time, businesses will manufacture and invest more locally to help offset both labor shortages and the nationalist and geopolitical pressures curbing globalized supply chains. That will increase production costs and local workers’ bargaining power. Global savings will fall as older people consume more than they produce, spending particularly on healthcare. All that will push up interest rates, he predicted.

A meeting of global central bankers in Jackson Hole, Wyoming, in August 2022 for the first time since 2019 found the bankers publicly reflecting a similar assessment, the Journal reported. “I don’t think that we are going to go back to that environment of low inflation,” European Central Bank President Christine Lagarde said on a panel.

7. The People Who Did All This Are Still in Charge

This reality applies to nearly every major political problem: The same people who have created these messes are the same people who largely retain the power to respond to them. The same people writing massive spending bills that divert our economy away from productive labor and into rent-seekers’ pockets are still largely in charge of government spending.

There might have been a slight shift of power in the House, but there hasn’t in the Senate, nor in the presidency. The same guy who claims the power to “pen and phone” a trillion dollars in student loan bailouts is in office, and all his K Street and Wall Street buddies still have gleefully effective access. You can be sure this cabal of crooks isn’t going to be looking out for your best interests now that we’re about to have a potentially dangerous recession.

That may be the most significant systemic reason to expect our markets to be heading for an even rougher ride in 2023 than we’ve had from 2020 to 2022.

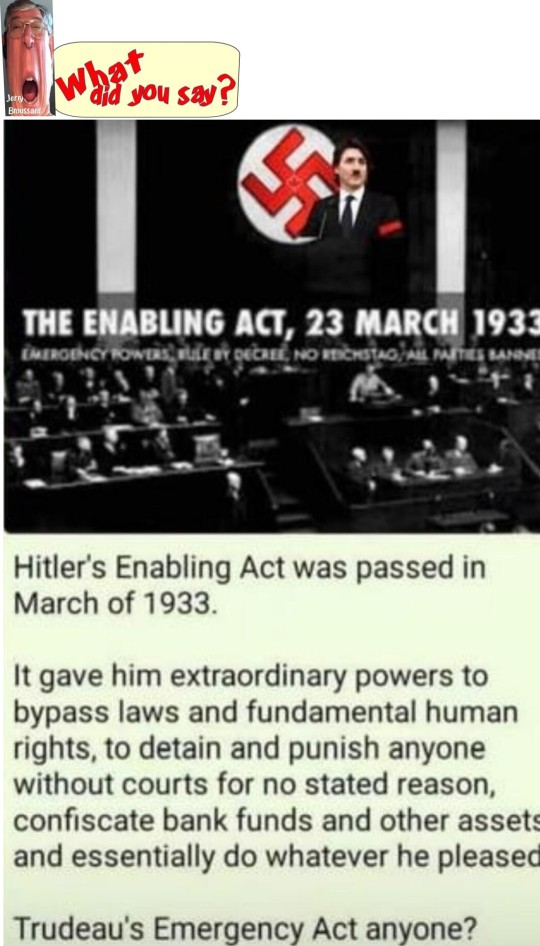

Last week, Canadian Prime Minister Justin Trudeau announced the suspension of Canadians’ rights last week in his invocation of the Emergencies Act to stop the Freedom Convoy protests in Ottawa and elsewhere. Among the restrictions announced are greater controls over the online crowdfunding sites that help to fund the protesters and attempts to control the flow of cryptocurrencies like Bitcoin. According to news reports, “credit card processors and fund-raising services will be required to report any blockade-related campaigns to Canada’s anti-money laundering agency.” Canadian banks quickly fell in line with the decrees, with Toronto-Dominion Bank freezing two personal bank accounts containing C$1.4 million ($1.1 million) they said was intended to support the truckers.

It bears a striking resemblance to the Biden administration’s recent efforts to intensely monitor what goes in and out of Americans’ bank accounts. The president’s expected announcement this week of an executive order to explore greater regulation of cryptocurrency is likewise an attempt to stick the state’s nose ever deeper into the average citizen’s business.

You Don’t Control Your Money Like You Used To

We’ve grown used to the idea that the government has a monopoly on money. Coining money is one of those powers of the state that most people never consider, like building roads or controlling national borders. Our money has dead presidents on it — it’s plainly a government operation. Where else would money come from, right?

But before the rise of electronic money transfers — the electronic bill-pay, direct deposit, and credit and debit card purchases we make every day now — whether the dollar bill in your wallet was issued by a bank (as in the early days of the republic) or by the Federal Reserve (as they are now) did not much matter. It was yours. No one knew what you spent it on unless you chose to tell them. That meant greater privacy, both from your neighbors and from your government. But it also entailed risk. Cash could be stolen, lost, or destroyed, and there was no way to get it back. And it was cumbersome, especially as inflation ate away at the value of a dollar. Could you bring cash for a down payment on a house? Sure. It still happens. But hauling a suitcase full of cash invites the scrutiny of thieves and the state — even when it’s completely legal.

The convenience of electronic money has been clear for decades now, but the dark side is showing itself this year like never before. All of the convenience of moving money around effortlessly comes at the cost of losing control over it.

How Goverment Uses Control of Your Money to Control You

These digital transfers feel, to most of us, like magic. A volley of ones and zeros flies through the cybernetic ether and — poof! — your electric bill is paid. But in truth, the data is routed through banks, and there are fewer of them all the time. Those remaining, many-times-merged financial giants that handle our affairs are, for all their clout and power, susceptible to government pressure.

We have seen it already when the Obama administration leaned on banks to refuse to deal with people involved in marijuana or the sex trade, even where those businesses were legal at the local level. No federal law gave them this power: the threat was enough. And where people keep money in cash, the government often finds a way to take it without even bothering to charge the owners with a crime.

Trudeau’s emergency measures take advantage of these pressure points and lean on banks to choke off the complete flow of money to and from those he deems enemies of the state. No charges, no trial, just shutting it down. Now Trudeau’s government wants to make these “temporary” measures permanent. The slippery slope is usually not so steep, but these are strange times.

Governments have always used the word “emergency” to do what they want and to trample the liberties of the dissenting minority. Control over our money makes that easier than ever. Even the more self-sufficient among us engage in trade and unless you choose to live like a hermit, money is a part of that.

How Crypto Challenges the Government Monopoly on Money

Governments understand that alternatives to state-issued money, like cryptocurrency, are a threat to that hegemony. Trudeau and Biden demonstrate that in their recent efforts to control Bitcoin and other cryptocurrencies. But the beauty of these new systems is that they are made, purposely, to be beyond the control of any person or government.

When Bitcoin launched more than a decade ago, most of us (myself included) barely understood what it was or how it worked. Fake money for dark web mischief, I figured, an eventual failure at best, a scam at worst. Yet here we are in 2022, where government-issued money is eroded by inflation and controlled by statist decrees. They leave peaceful opponents with a choice between the old (gold) or the new (crypto). And crypto is a heck of a lot easier to carry around.

In deciding an earlier banking law question in McCulloch v. Maryland in 1819, Chief Justice John Marshall said that “the power to tax involves the power to destroy.” Two centuries on, we could apply a modern twist: the power to regulate involves the power to control.

Cryptocurrency was just a passing fad until government overreach made it a necessity. Decades of deficit spending have inflated the currency and decades of creeping statism have given the government massive power over how money is used. The government’s monopoly on money has failed and, like it or not, cryptocurrency is at least part of the answer.

Kyle Sammin is a senior contributor to The Federalist, the senior editor of the Philadelphia Weekly, and the co-host of the Conservative Minds podcast podcast. Follow him on Twitter at @KyleSammin.

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

NEWSMAX

News, Opinion, Interviews, Research and discussion

Opinion

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

You Version

Bible Translations, Devotional Tools and Plans, BLOG, free mobile application; notes and more

Political

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

NEWSMAX

News, Opinion, Interviews, Research and discussion

Spiritual

American Family Association

American Family Association (AFA), a non-profit 501(c)(3) organization, was founded in 1977 by Donald E. Wildmon, who was the pastor of First United Methodist Church in Southaven, Mississippi, at the time. Since 1977, AFA has been on the frontlines of Ame

Bible Gateway

The Bible Gateway is a tool for reading and researching scripture online — all in the language or translation of your choice! It provides advanced searching capabilities, which allow readers to find and compare particular passages in scripture based on

You must be logged in to post a comment.