Joe Biden Met with Hunter’s Business Associates More Times Than with His Cabinet

By: M.D. Kittle | December 20, 2024

Read more at https://thefederalist.com/2024/12/20/joe-biden-met-with-hunters-business-associates-more-times-than-with-his-cabinet/

M.D. Kittle

They say the U.S. presidency is the loneliest job in the world. Maybe the second-loneliest gig is that of Cabinet secretary in President Joe Biden’s administration.

A piece published Thursday in the Wall Street Journal pulls from dozens of sources who say Biden’s inner circle of trusted aides increasingly kept contact with the president at a minimum, including the people he should have depended on most to consult and advise for the good of the nation.

The president who has spent a good chunk of his term out of the office apparently was not all that keen on meetings with his Cabinet secretaries. In fact, Biden may have met more often with his criminal son’s sketchy clients than he has with his administration’s top managers.

‘Hide the President’s True Condition’

Joe Biden was such a political liability that his handlers hid him away during the 2020 presidential campaign. The man campaigned from his Delaware basement through the brunt of the election year. The cloistered strategy wasn’t as much about protecting the feeble geezer from Covid as it was designed to prevent American voters from seeing what a physical and mental mess Biden really was.

Even the Pravda Press, which was openly rooting for — and covering for — the Democrat gaffe machine, was forced to report on Biden’s bunker campaign.

“Over the past six weeks, presumptive Democratic presidential nominee Joe Biden has been running his campaign from his Delaware basement,” CBS News reported in April of 2020, showcasing a fluff piece from The New York Times about how team Biden was attempting to “keep his campaign relevant during the pandemic.”

The occasional programmed Zoom calls notwithstanding, keeping Biden “relevant” (or electable), meant keeping him hidden — literally underground.

That limited contact strategy has defined the octogenarian’s presidential tenure. Biden has held the fewest number of press conferences and media interviews of any president since Ronald Reagan’s first term, and it isn’t close, Axios reported in late June. The publication at the time noted that Biden was about to sit for a “rare interview with ABC News” … “amid growing concern about his age and acuity — and accusations that his inner circle has taken pains to hide the president’s true condition from public view.”

Quaintly, back then Axios and its corporate media bedfellows were still trying to convince Americans not to believe their lying eyes, that there were “two Bidens”: the 81-year-old who had recently froze up like so much freezer peas in his debate with former President Donald Trump, and the virile campaigning Joe.

‘Wouldn’t be Welcome’

It turns out, Biden wasn’t just hiding from voters. He was ducking his own Cabinet.

“Interactions between Biden and many of his cabinet members were relatively infrequent and often tightly scripted. At least one cabinet member stopped requesting calls with the president, because it was clear that such requests wouldn’t be welcome, a former senior cabinet aide said,” reports The Wall Street Journal in a piece headlined, “How the White House Functioned With a Diminished Biden in Charge.”

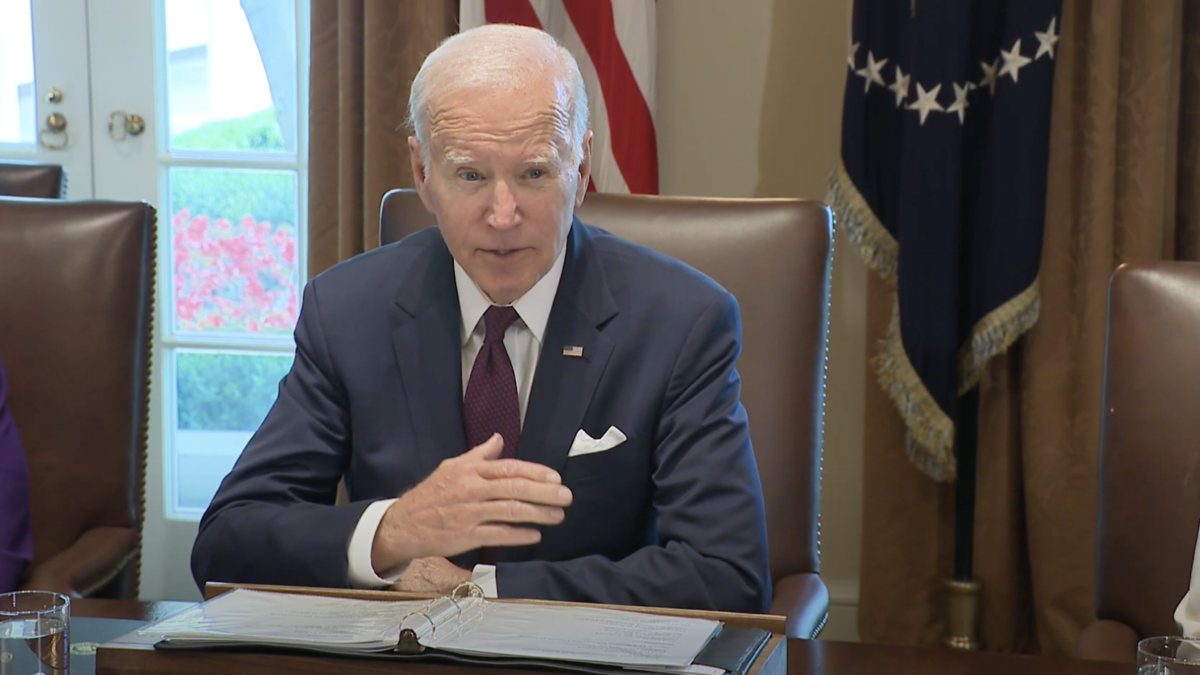

The story further noted that “cabinet members — including powerful secretaries such as Defense’s Lloyd Austin and Treasury’s Janet Yellen — were infrequent or grew less frequent. Some legislative leaders had a hard time getting the president’s ear at key moments, including ahead of the U.S.’s disastrous pullout from Afghanistan.”

Like other aging, cognitively diminished seniors, Biden had his “good days, and bad days,” one former aide told the publication. The president has routinely gotten a pass from fellow Democrats and corporate media on his memory lapses, mumbled and jumbled answers to questions, and outright lies. Remember, Special Counsel Robert Hur’s report detailing Biden’s possession and mishandling of classified documents recommended the president not be prosecuted because a jury might well see him as a “sympathetic, well-meaning elderly man with a poor memory.”

Meeting with the ‘Big Guy’

But as The Federalist has reported, said “well-meaning elderly man” is alleged to have interacted with Hunter Biden’s suspect clients “countless times.” Devon Archer, the younger Biden’s former business associate, testified before a congressional committee last year that Hunter put his father, vice president at the time, on speakerphone nearly two dozen times while talking to overseas business contacts. Archer discussed Hunter’s involvement on the board of Ukrainian natural gas company Burisma Holdings and the hefty checks it wrote to a guy seemingly unqualified for the job. Archer and others have alleged Burisma and other “clients” were paying for the Biden “brand.” Aka, access to the vice president.

“Burisma would have gone out of business if ‘the brand’ had not been attached to it,” the New York Post reported, quoting from a readout from panel Republicans.

“Archer talked about the ‘big guy’ and how Hunter Biden always said, ‘We need to talk to my guy,’ ‘We need to see when my guy is going to be here,’ and those types of things,” Rep. Andy Biggs (R-Ariz.) told reporters as he left the deposition in July 2023.

There were many more interactions between Vice President Joe Biden and his son’s other business associates, according to the laptop that the Deep State and the accomplice media long claimed did not exist. As The Federalist’s Tristan Justice reported:

Biden reportedly met with Ukrainian, Russian, and Kazakhstani business partners at a famous D.C. establishment in 2015. The meeting, arranged by Hunter, took place at one of Georgetown’s most famous restaurants, Café Milano… Vadym Pozharskyi, an executive at the Ukrainian energy company Burisma, thanked Hunter for the introduction to his father.

“Dear Hunter, thank you for inviting me to DC and giving an opportunity to meet your father and spent [sic] some time together,” Pozharskyi wrote in an email released by the New York Post weeks before the 2020 election.

And visitor logs show Hunter Biden’s business pals paid a call on the White House at least 80 times while Biden was VP, Fox News reported. A meeting with the elder Biden at the time involved Chinese businessmen tied to a firm that Hunter Biden had invested in.

Earlier this month, the president issued a sweeping, unprecedented pardon of his multi-felon son, not merely for the serious crimes for which he was found guilty but for crimes that he may have committed during his salad days with Burisma and the other business associates seeking access to the “Big Guy.”

The Disaster of Absence

As president, Biden has held just nine full Cabinet meetings, the Wall Street Journal reported. The numbers include three such sessions in 2021, two in 2022, three in 2023 and only one this year. By comparison, President Barack Obama led 19 Cabinet meetings and President Donald Trump called 25 in their first terms, the Journal noted, using data obtained by former CBS News reporter Mark Knoller.

While White House officials have disputed Biden’s distance and decline, the cloistering of the cognitively slipping president appears to have contributed to some disastrous consequences.

Rep. Adam Smith, a Washington Democrat who chaired the House Armed Services Committee in 2021, told the Wall Street Journal that he was shut out of conversations with the president leading up to the administration’s debacle of a withdrawal from Afghanistan.

“I was begging them to set expectations low,” Smith, who had misgivings about how the operation would go, told the publication.

The Journal reported that “[f]ormer administration officials said it often didn’t seem like Biden had his finger on the pulse.” Many of us have often been left wondering if the president has had a pulse at all.

Witness accounts and his degenerate son’s own emails suggest Biden had plenty of vim and vigor when it was time to talk about corrupt financial deals. It was the business of protecting and leading America that he seemed disinterested in during his historically awful presidential term.

You must be logged in to post a comment.